Why it matters: Toto's advanced ceramics division – not its well-known bidet toilets – is increasingly drawing the attention of investors who view the Japanese manufacturer as a quiet but important player in the global race to build AI-era memory chips. A campaign by UK-based activist fund Palliser Capital is now pushing that low-profile segment into the spotlight, arguing that the company's wafer-handling technology has become strategically significant for NAND flash manufacturing and, by extension, AI infrastructure.

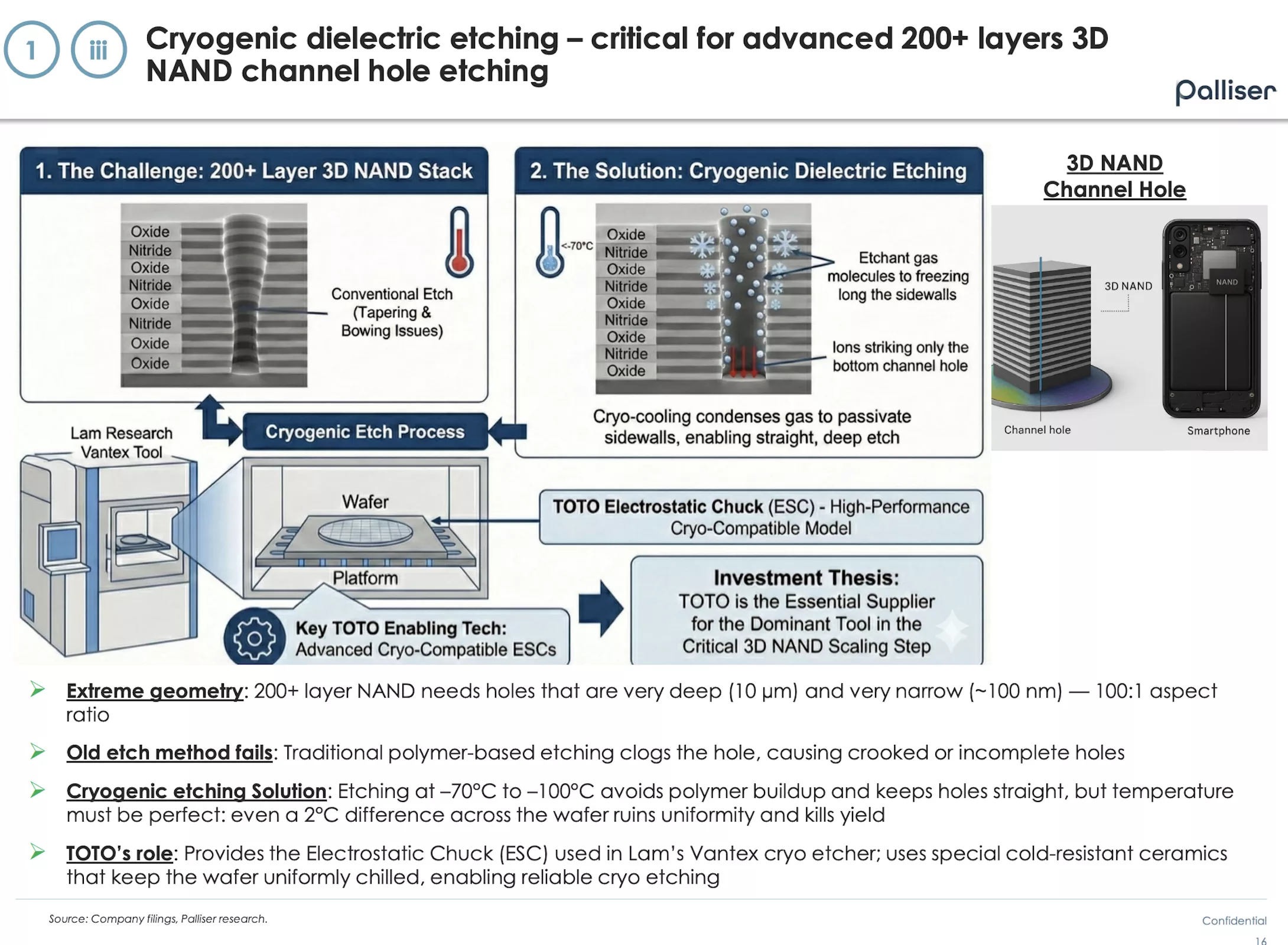

Behind the investor interest is a highly specialized component: electrostatic chucks, or ESCs, used in semiconductor etch tools to hold wafers flat, clean, and thermally stable while they are bombarded with plasma.

Unlike mechanical clamps, ESCs use electrostatic force within specialized ceramic materials to hold the silicon wafer firmly against the chuck, maintaining even contact and reducing bending, particles, and contamination during demanding process steps. In advanced 3D NAND production, these chucks are critical components of cryogenic etch tools that carve extremely deep, narrow channels through stacks of more than 200 layers.

Toto's ceramics are engineered to remain stable at very low temperatures – an essential requirement for cryogenic etching, which operates far below room temperature to produce cleaner sidewalls, reduce defects, and maintain tighter control over feature geometry as layer counts increase. The company's ESCs combine cold-resistant ceramics with integrated heaters and cooling channels to keep the wafer surface at a highly uniform temperature, even when exposed to intense plasma, high voltage, and vacuum conditions. That combination enables equipment vendors to meet stringent uniformity specifications as NAND manufacturers push channel depths and density ever higher.

The shift may appear abrupt from the outside, but Toto has spent decades building expertise in high-performance ceramics – initially for sanitary products and industrial applications, and later for precision components.

Over time, that work expanded into a portfolio that extends well beyond bathroom fixtures to include air bearings, bonding capillaries, and structural parts for semiconductor manufacturing equipment that must withstand thermal stress and tight mechanical tolerances.

Electrostatic chucks have been part of the company's portfolio since the 1980s, but only in recent years have they become significant contributors to earnings as demand for advanced memory and logic manufacturing has accelerated.

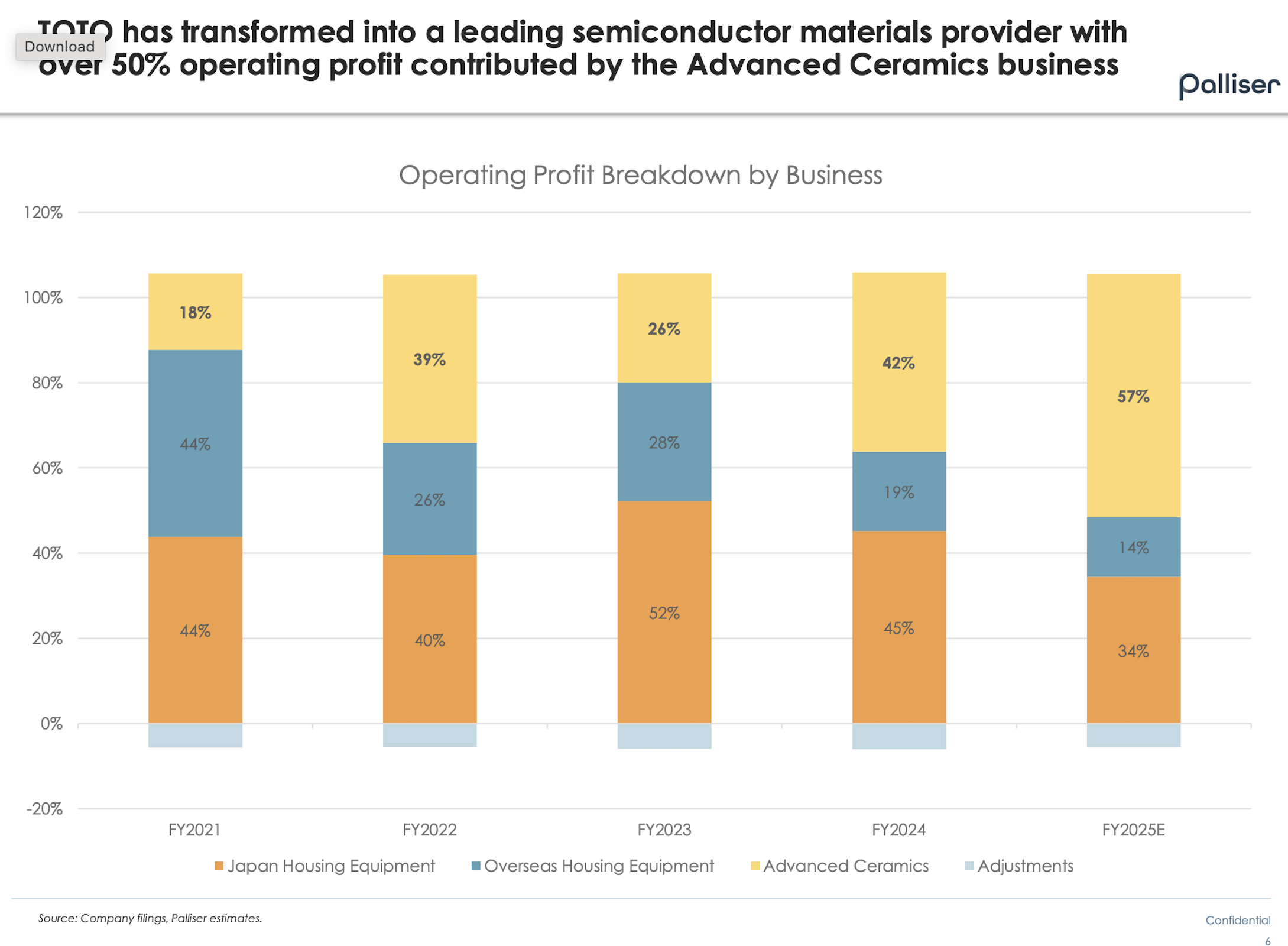

That evolution has reshaped the company's earnings mix. Toto's so-called advanced ceramics segment now accounts for roughly 40 percent of operating profit, and recent materials from both activists and the company suggest its contribution may have risen to more than half of total operating income.

Yet the brand remains globally associated with heated toilet seats and Washlet bidets, obscuring the extent to which it has, in Palliser's words, "quietly evolved from a traditional domestic sanitary ware champion into a rising powerhouse in advanced ceramics for semiconductor manufacturing."

The timing of this renewed attention is not accidental. As hyperscalers and AI-focused companies expand capacity, memory manufacturers have resumed capital spending cycles that were previously delayed, directing more budget toward advanced etch, deposition, and packaging equipment required for 3D NAND and other high-density devices.

Palliser's thesis is that this backdrop positions Toto as "the most undervalued and overlooked AI memory beneficiary," since its ceramics-based chucks are closely tied to NAND technology roadmaps rather than general industrial demand.

The fund argues that cryogenic etching will grow increasingly important as NAND architectures become more layered and complex, potentially expanding Toto's addressable market and giving it what the investor describes as a five-year competitive moat before rivals can replicate its combination of materials science, design expertise, and manufacturing capabilities.

Palliser's campaign focuses less on altering Toto's product strategy and more on capital allocation and investor communication. The fund is urging the company to provide more granular disclosure about its advanced ceramics business so that the market can better evaluate its margins, growth trajectory, and competitive positioning. It also contends that too little of Toto's planned investment is directed toward the higher-return ceramics segment and is advocating for a capital allocation framework that prioritizes that unit.

The market has already begun to reprice Toto based on its semiconductor exposure. Over the past year, the stock has risen more than 60 percent, including a single-day gain of over five percent after news of Palliser's stake first emerged.

Still, some of the more aggressive claims about a multi-year technological moat and rapid revenue growth remain, at this stage, part of an activist narrative rather than an independent market consensus. Palliser's materials project revenue growth of 30 percent or more for the advanced ceramics segment over the next two years, driven by the NAND upgrade cycle and steady replacement demand. However, that forecast is based on the fund's own modeling and aligned with its investment incentives.

Electrostatic chucks are clearly essential to advanced, low-temperature etch processes. Whether that importance translates into an outsized growth surge for Toto, however, depends on how aggressively memory manufacturers execute their capacity expansion plans over the coming years.

Suddenly Toto's most valuable business isn't toilets, but chipmaking ceramics