TL;DR: The rollout of small modular reactors will likely be shaped as much by policy, economics, and regulation as by engineering advances. While they promise a new era for nuclear energy, unresolved questions around cost, safety, and long-term public acceptance remain major hurdles.

As the demand for cleaner energy grows, small modular reactors (SMRs) are drawing fresh attention, investment, and regulatory scrutiny. Though the idea dates back to the earliest days of commercial nuclear power, engineers in the 1960s pivoted toward ever-larger plants, betting that scale would deliver higher efficiency and lower costs.

Now, decades later, the industry is revisiting smaller designs. Advocates argue SMRs could be sited closer to population centers and industrial hubs, cutting the need for vast transmission networks and enabling new applications – from steelmaking and desalination to powering remote mines.

Unlike conventional nuclear plants, SMRs are factory-built in modules and assembled on-site, a shift intended to shorten construction timelines and improve cost predictability. Their modular design allows operators to scale capacity gradually to meet rising demand and tailor installations to specific sites or industrial partners.

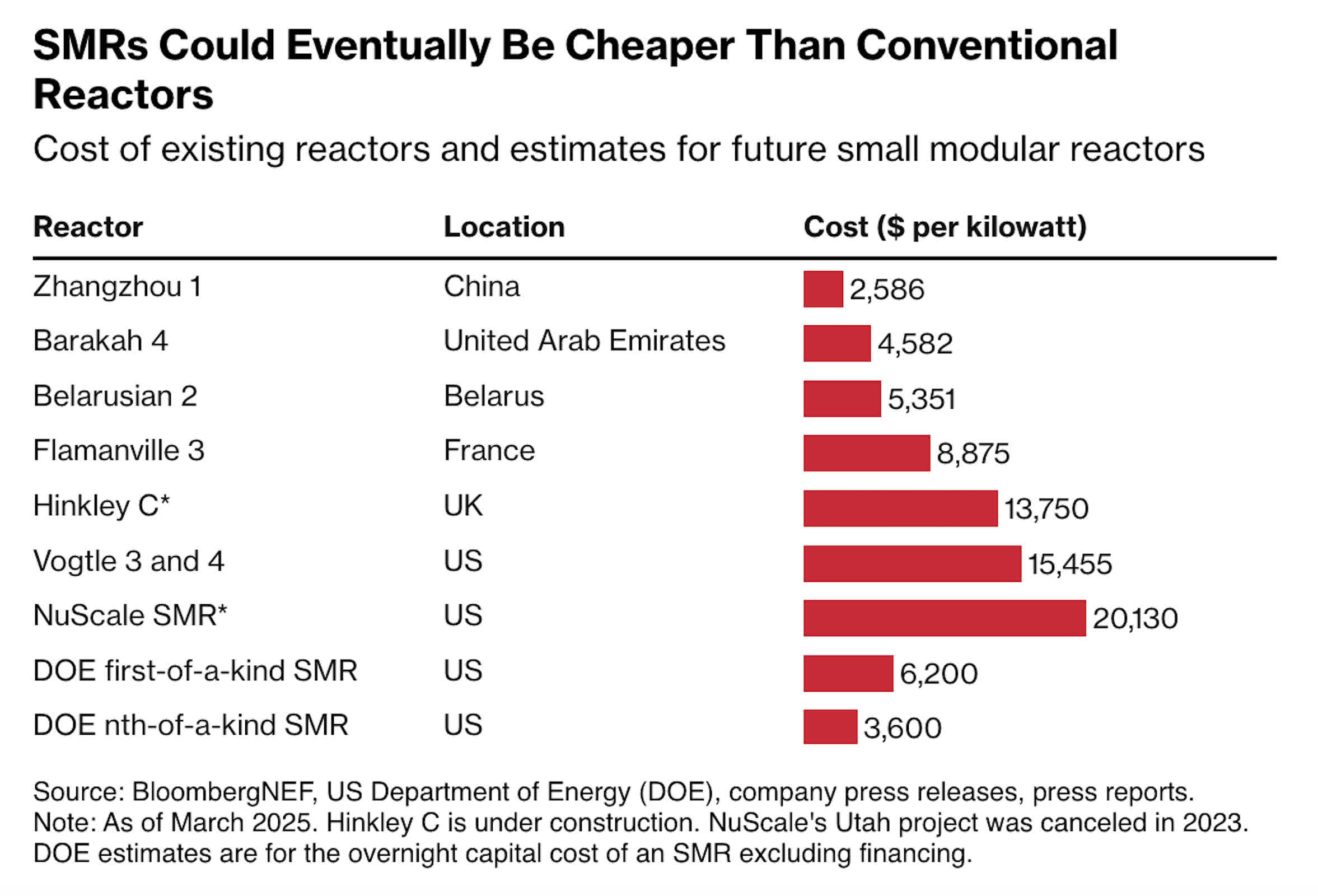

Crucially, the approach is meant to avoid the overruns and years-long delays that have dogged traditional projects, such as the Vogtle 3 and 4 reactors in Georgia, which came online seven years late at more than double their original $14 billion budget.

A defining feature of SMRs is the diversity of designs and fuels under development. Of the 127 unique concepts tracked worldwide, many rely on novel fuels like those with higher uranium isotope concentrations that support hotter and longer operation between refuelings.

While attractive to potential customers, these innovations face steep regulatory hurdles. Each reactor's safety case and fuel type must undergo exhaustive certification, often stretching over years or even decades.

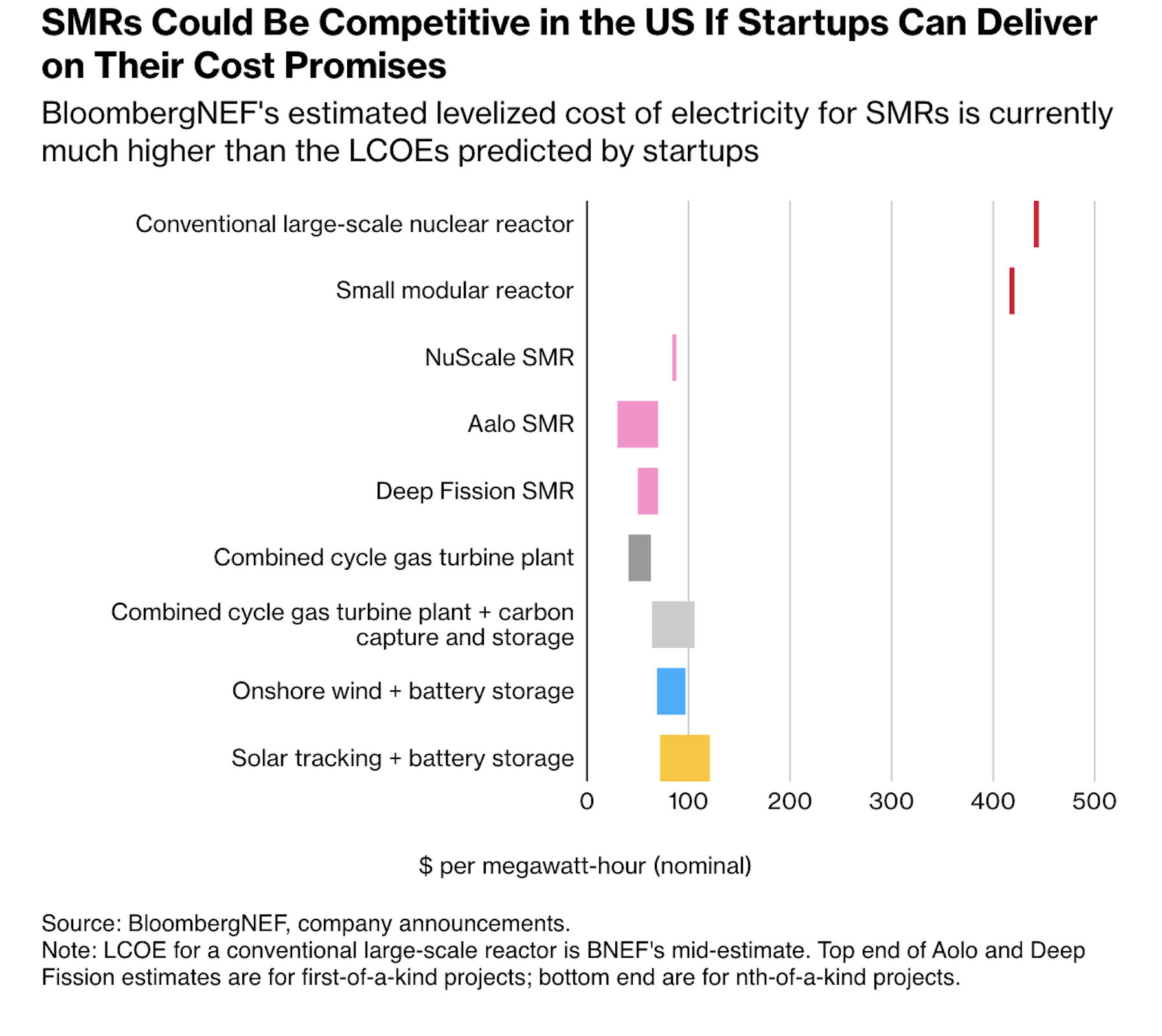

Despite rising policy support and private investment, SMR economics remain uncertain. Proponents argue that standardized, mass-produced modules will ultimately cut costs below those of legacy nuclear plants, yet real-world data is scarce.

NuScale, the company once expected to deliver the first US commercial SMRs, scrapped its six-reactor Carbon Free Power Project in Utah in 2023 after costs surged and utilities hesitated to commit. The projected price of power rose to $89 per megawatt-hour – well above earlier estimates, and higher than both new natural gas generation and wind or solar power paired with battery storage, according to BloombergNEF.

High costs and lengthy approval timelines are fueling calls for consolidation in the SMR sector to pare back less-viable designs. NuScale's own experience underscores the challenge. The company spent more than three years and over $500 million to secure US authorization for its 60-megawatt reactor configuration.

As of late 2025, only two SMR projects are in commercial operation worldwide. Russia's Rosatom runs a pair of 35-megawatt reactors mounted on a floating platform supplying power to Arctic communities, completed in 2020. In China, China National Nuclear Corporation (CNNC) commissioned two 100-megawatt units at Shidao Bay in 2023. Beyond these early deployments, dozens of new projects are in planning or under construction globally.

The next wave of SMR development is being led by state-backed giants such as Électricité de France, Rosatom, and CNNC, alongside US-based ventures like TerraPower – founded by Bill Gates – and PacifiCorp, part of Warren Buffett's Berkshire Hathaway. TerraPower has begun site preparation at a former coal plant in Wyoming, though its sodium-cooled 345-megawatt design still awaits regulatory approval.

Interest from the technology sector is growing rapidly, as data center operators face soaring energy demand and intensifying scrutiny over carbon emissions. Amazon, Google, and Oracle are reportedly exploring SMRs to power their expanding networks. BloombergNEF estimates that US data centers could consume about nine percent of national electricity by 2035, up from roughly four percent today.

In October, Google announced an agreement with Kairos Power to secure nuclear energy, targeting up to 500 megawatts from Kairos' SMRs, with first generation planned for 2035 in Tennessee. Equinix committed in 2024 to purchase 500 megawatts from SMR startup Oklo – backed by OpenAI's Sam Altman – and pre-ordered 20 microreactors from California-based Radiant Nuclear. Still, the US Nuclear Regulatory Commission has not licensed any domestic SMR project to date.

President Trump has voiced support for expanding US nuclear capacity, including SMRs. In March, the Department of Energy revived a $900 million SMR funding program, building on earlier grants such as $2 billion for TerraPower's Wyoming project under a cost-sharing agreement. In May, Trump signed executive orders to streamline regulatory approvals and accelerate efforts to quadruple US nuclear capacity to 400 gigawatts by 2050. DOE test runs of new SMR fuels are scheduled to begin in 2026.

International cooperation is also advancing. During a September state visit to Britain, the US and UK signed a memorandum of understanding to coordinate regulatory processes and accelerate SMR permitting, including reciprocal use of safety reviews. Rolls-Royce, named the UK's preferred SMR developer in June, is pursuing approval in both countries and stands to benefit from Britain's £2.5 billion public funding pledge, with its first domestic station targeted for mid-2030s operation.

Safety remains a point of contention. Advocates argue that advanced SMRs incorporate passive safety systems such as molten salt or liquid metal coolants and lower operating pressures, reducing reliance on pumps or operator intervention. Critics counter that siting reactors closer to population centers introduces new risks, while the long-standing problem of managing radioactive waste remains unresolved across all reactor types.

Image credit: Bloomberg