Everything is Getting Worse: Research firm Omdia has released its latest figures on the state of the PC market. Conditions are deteriorating, hardware prices continue to rise amid AI-driven demand, and consumers are holding off on buying new PCs for the time being – though there are a few notable exceptions.

Omdia recently reported that PC shipments in the US fell 7% year over year in the first quarter of 2026. The London-based research firm estimates that 15.8 million PCs were shipped to the US market during 1Q26, marking the steepest annual decline since the third quarter of 2023. The weak market is being driven by several factors, with AI-related demand likely playing the biggest role.

Heavy spending by Big Tech companies and AI firms is putting significant pressure on the supply chain, causing storage and memory prices to continue rising. As a result, PC manufacturers – and many other hardware vendors – have been forced to pass those higher costs on to consumers. Omdia also said the "demand hangover" associated with the Windows 11 upgrade cycle has largely run its course. Meanwhile, the inventory buildup driven by Trump's 2025 tariffs is no longer a significant factor.

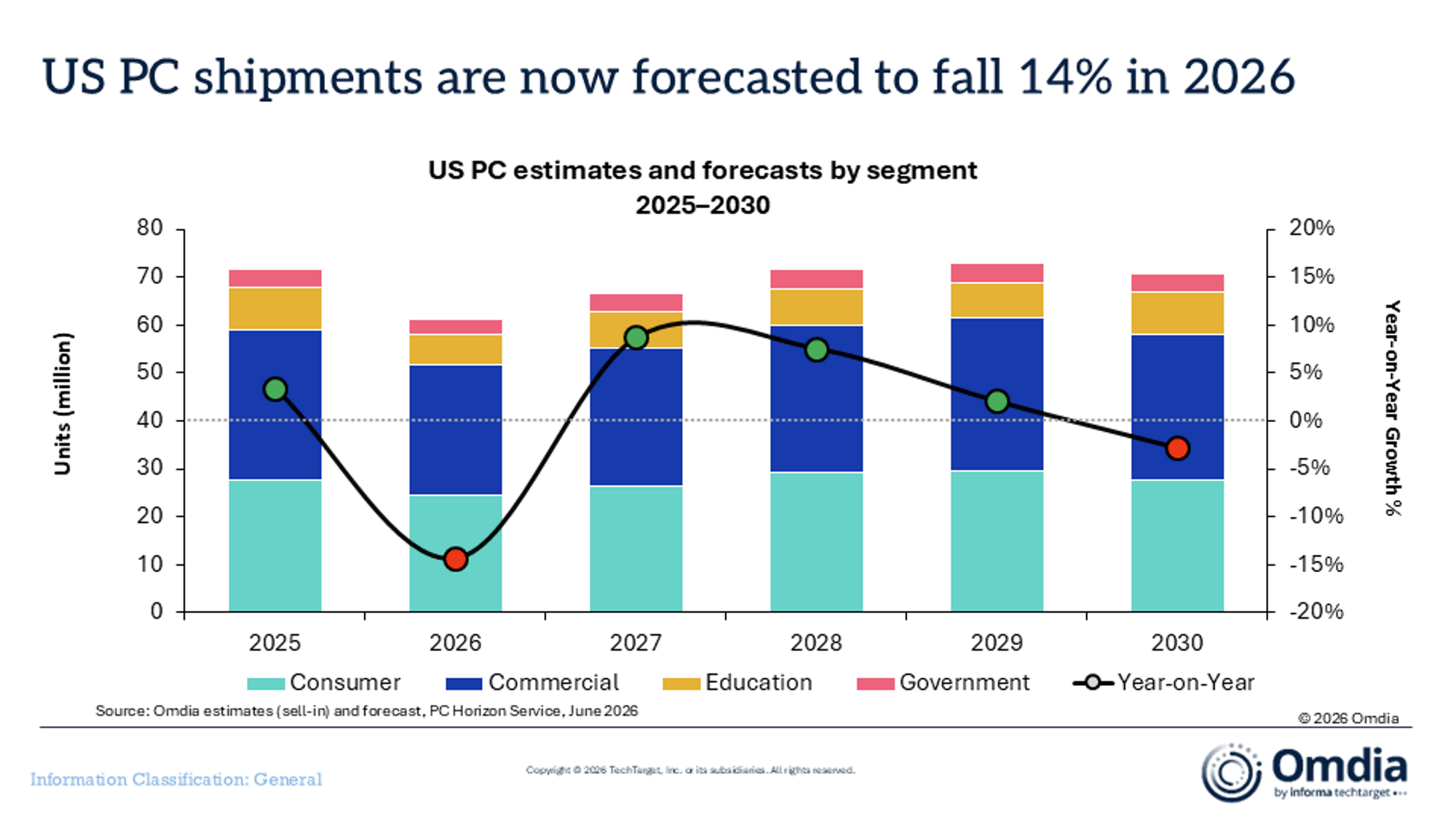

The rising cost of memory chips and storage devices has largely eroded profit margins on entry-level PCs, which is why shipments of systems priced below $500 declined 18.7% year over year. Omdia now expects PC shipments to continue falling throughout the year, forecasting a total decline of 14.4% in 2026 compared to 2025.

According to Omdia Senior Analyst Scott Braverman, the consumer PC market experienced a significantly steeper decline than the commercial segment. Consumer PC shipments fell 9.5% year over year, while commercial shipments declined "only" 5% during the quarter. Business PCs are holding up better thanks to the ongoing Windows 11 refresh cycle and inventory stockpiling ahead of further price increases.

Budget-constrained segments, including government procurement and education, experienced a slightly steeper decline than the commercial market. Both are expected to remain under pressure through the end of the year, although Omdia believes they could see a meaningful recovery in 2027.

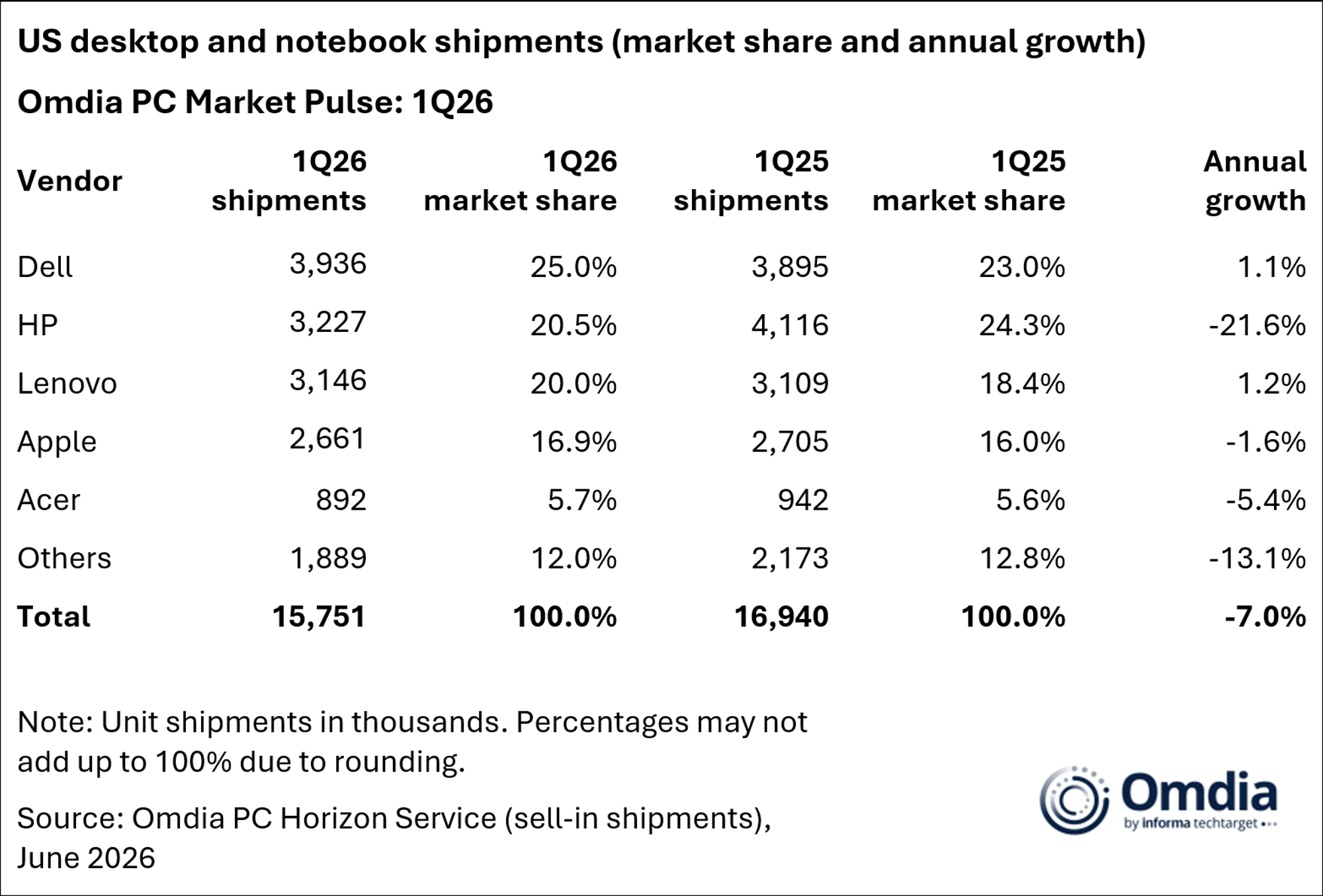

Omdia also recorded significant performance variation among vendors active in the US market. Volatile pricing conditions contributed to a sharp decline for HP, which saw shipments fall 21.6% and lost its position as the largest vendor in the US, holding a 20.5% market share. Dell overtook HP to become the leading US vendor, posting 1.1% growth and a 25% market share.

Lenovo shipments also grew 1.2% during the quarter, making the Chinese OEM the third largest vendor in the US with a 20% market share. Apple, Acer, and other smaller manufacturers saw declines of 1.6%, 5.4%, and 13.1%, respectively. Smaller OEMs in particular are facing the most challenging conditions, as they have limited leverage when negotiating component procurement.