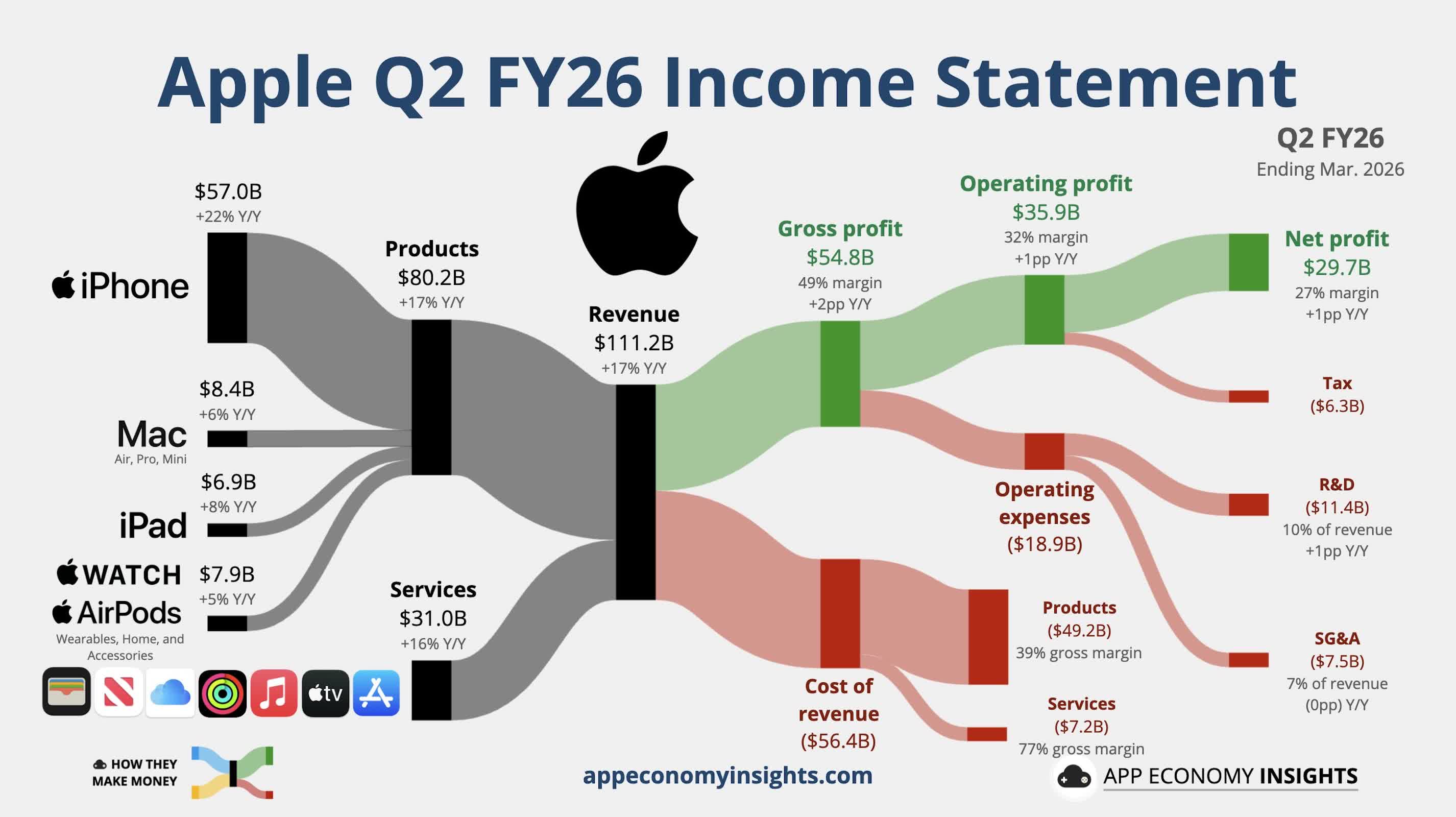

Bottom line: Apple's latest earnings highlight a now-familiar problem: it can build demand faster than its supply chain can keep up. The company posted $111.18 billion in revenue for the fiscal second quarter that ended March 28, topping expectations and delivering what CEO Tim Cook described as its best March quarter ever. Earnings came in at $2.01 per share, also ahead of forecasts. Apple's stock rose nearly 4% in after-hours trading as investors reacted to the results, a stronger-than-expected outlook, and a new $100 billion share buyback program.

The quarter showed how dependent Apple has become on its silicon strategy. The iPhone 17 lineup, built on advanced processors made by TSMC using a variant of the manufacturing technology behind leading AI chips, continues to drive the bulk of revenue. iPhone sales reached $56.99 billion, slightly missing estimates, but not for lack of demand.

"The demand was off the charts. And there's just a little less flexibility in the supply chain at the moment for getting more parts," Cook told Reuters.

That constraint reflects pressure on advanced chip production, where AI workloads and high-performance computing are competing for the same manufacturing capacity. Apple is feeling that pressure directly, and it may not be limited to iPhones. Cook said on the earnings call that supply constraints could also affect Mac shipments, given continued strong demand.

Credit: App Economy Insights

Newer products are adding to that demand, particularly the MacBook Neo. The device, which starts at $599 and runs on an A18 Pro chip, represents a shift toward lower-cost systems without abandoning Apple's in-house silicon approach. It helped push Mac revenue to $8.4 billion, ahead of expectations, marking Apple's push into territory dominated by Chromebooks and budget Windows laptops.

Apple's services business continues to grow as well. Revenue from services hit $30.98 billion for the quarter, exceeding estimates and setting another record. The segment remains a critical margin buffer, especially as hardware costs rise. China was another bright spot, with revenue of $20.5 billion, also ahead of expectations.

Cost pressures, however, are beginning to show. Apple reported gross margins of 49.27%, better than analysts expected, largely because it was still working through previously purchased memory inventory. That advantage is fading. The company expects margins to dip to 47.5% – 48.5% in the current quarter as memory prices rise.

"We expect significantly higher memory costs," Cook said on the earnings call. "Where we don't give color beyond June, I can tell you that beyond the June quarter, we believe memory costs will drive an increasing impact on our business."

Even with those pressures, Apple is continuing to spend heavily on future products. Research and development costs climbed 33.5% year over year to $11.42 billion, reflecting ongoing investment in AI and custom silicon. More details are likely to come in June at Apple's Worldwide Developers Conference, where the company is expected to outline updates to Siri and broader AI initiatives.

This comes as Apple prepares for a leadership transition. Cook is set to step down as CEO in September, with hardware chief John Ternus taking over. Cook will remain involved as executive chairman.

Apple is also rethinking how it manages its balance sheet. Chief Financial Officer Kevan Parekh said the company will no longer aim to reach a net cash-neutral position, a goal it had pursued since 2018. D.A. Davidson analyst Gil Luria said the move was likely intended to give Apple greater financial flexibility.

For the current quarter, Apple expects revenue growth between 14% and 17%, well above Wall Street projections. The forecast suggests that, even with supply constraints and rising component costs, demand for its latest devices – driven in large part by its chip roadmap – remains strong.

Apple's success is running into a familiar problem: not enough chips