Over the past few years, U.S. policymakers have developed a high degree of anxiety about America's need for onshore, leading-edge fab capabilities. The press has been filled with stories about all the ways the U.S. has fallen behind, how we can no longer produce chips at the leading edge. This anxiety is rooted both in geopolitical concerns around the rivalry with China and in worries that the U.S. has somehow lost the ability to produce chips, much like we seem to have lost the ability to manufacture many things.

We would argue that the problem is very much an economic one rather than a technological one.

Editor's Note:

Guest author Jonathan Goldberg is the founder of D2D Advisory, a multi-functional consulting firm. Jonathan has developed growth strategies and alliances for companies in the mobile, networking, gaming, and software industries.

Put simply, Intel can produce leading-edge semiconductors today; they just cannot do so economically. They have the know-how and the equipment. Their shortcomings are entirely based on the fact that they cannot yet make 18A, 3nm chips profitably.

Consider for a moment everyone's favorite fear-mongering scenario – what if the U.S. lost access to TSMC's Taiwan fabs? War, blockade, alien invasion – whatever the reason. And along with that, imagine the U.S. faced some military conflict, and the lack of leading-edge chips became an acute national security problem.

That would obviously cause immense disruption to the economy, but how long would it take for Intel to get its process working? It's reasonable to assume that the government could throw enough money at Intel to get its process up and running very quickly.

At first, Intel's yields would be terrible, and the government would effectively be covering those losses – paying fixed prices for wafers with only 5% or 10% good die. In semis, volume solves a lot of problems, and in a time of great need, they could afford all the bad wafers it would take to get enough learning under their belt to improve those yields.

The traditional narrative on TSMC's rise to success is that Intel missed the boat on mobile, TSMC became the foundry of choice for phones, and that drove their volumes.

Obviously, that is not a scenario anyone hopes for, but we mention it here because it speaks to an important but largely ignored reality today. The traditional narrative on TSMC's rise to success is that Intel missed the boat on mobile, TSMC became the foundry of choice for phones, and that drove their volumes.

With that volume, they were able to learn faster than others and, over time, win process leadership. All that is true, but it misses one critical factor. During that period, TSMC enjoyed massive subsidies. The best-known of those were direct subsidies from the Taiwan government, which allowed them to import wafer fabrication equipment in the early days. But a far bigger subsidy was indirect – the undervalued New Taiwan Dollar.

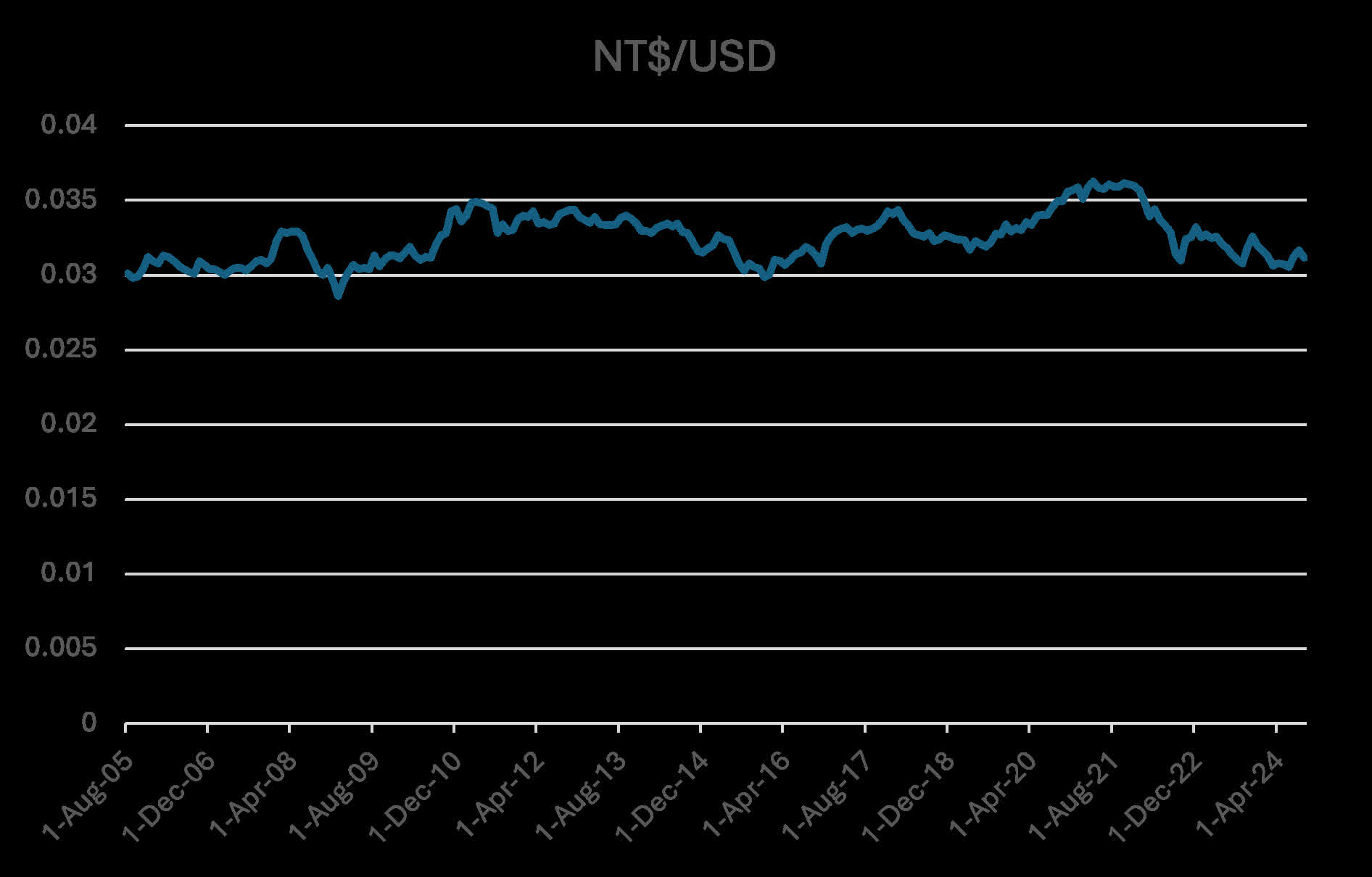

Historical NT$ / US$ Exchange Rate. Source: Investing.com

The NT$ is ostensibly a free-floating currency, but as the graph above shows, it appears to have been fixed to the U.S. dollar for over 20 years. Economist Brad Setser has written extensively about the mechanisms Taiwan uses to achieve this (TL;DR – commercial banks, then life insurance companies), essentially managing the currency to keep Taiwan competitive.

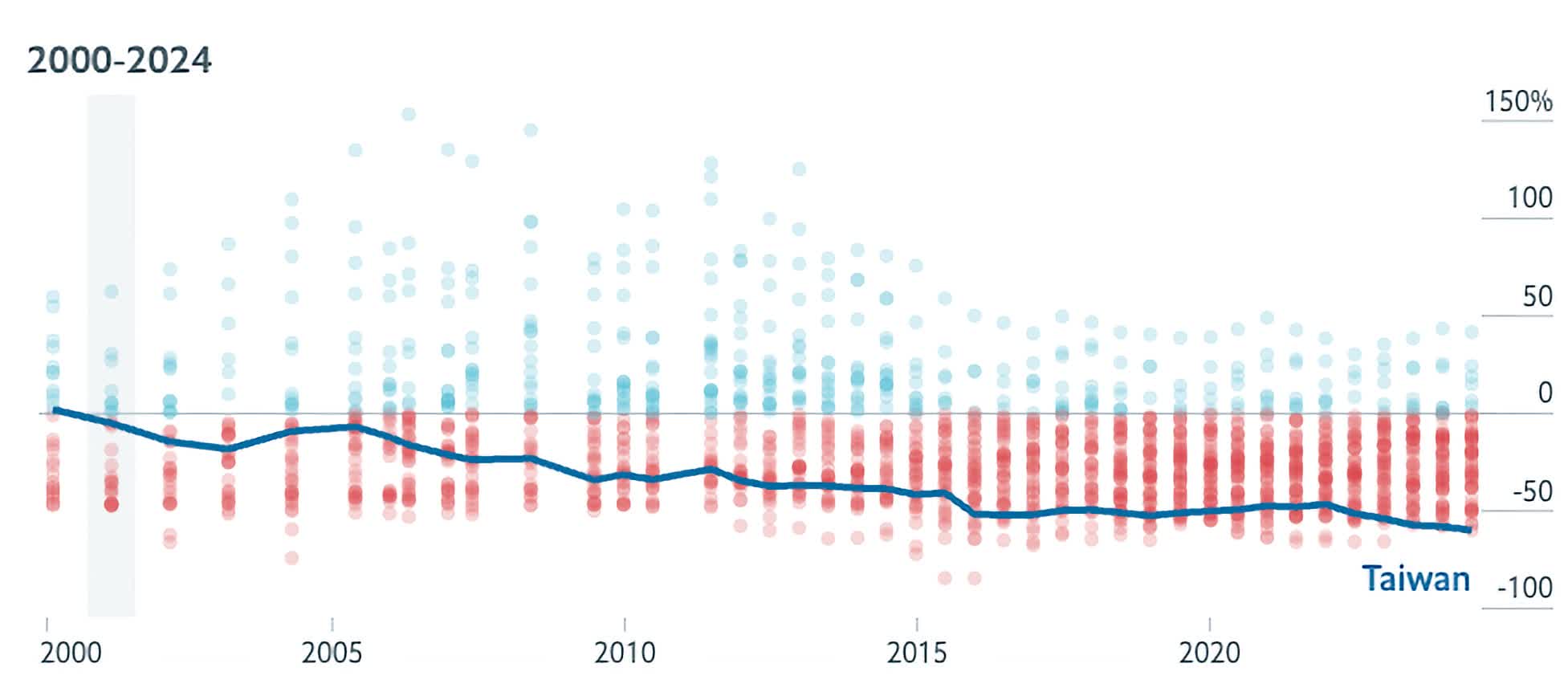

During this period, the U.S. dollar has inflated considerably, which effectively means the NT$ has fallen in value as well. The best way to demonstrate this is the Economist's Big Mac Index.

Source: Economist Big Mac Index. Blue Line is NT$

This is a handy way to show the degree to which a currency is under- or overvalued relative to the U.S. dollar. As this graph shows, the NT$ has steadily eroded in value against the U.S. dollar for the past twenty years, exactly the time when TSMC was rising. From what we understand, this decline really began with the Asian Financial Crisis in 1998 and has only grown over time.

This provides a massive, indirect subsidy to TSMC. They can pay their employees wages that are competitive in Taiwan but are effectively much less than what their competitors in the U.S. would have to pay.

TSMC's revenues are priced in U.S. dollars, but its workforce is paid in NT$, and they are the company's true asset. And this discount has been compounding for decades. We tend to think of devalued currencies as providing a way for exporters to undercut foreign competitors by offering lower prices. Instead, TSMC used the effects of that currency suppression to invest in its own talent pool.

We have read research that shows the NT$ is effectively underpriced by around 30% (using a more comprehensive method than the Big Mac Index, which shows a >50% level). So, we think it's no coincidence that TSMC has said its U.S. plant would be 20%-30% more expensive than its Taiwan fab's wafer costs.

To be clear, we are not diminishing TSMC's technical talent. They have immense capabilities and unrivaled human capital. But we think it's important to understand how they achieved those. TSMC management's true power move was investing their currency advantage into their own talent pool, rather than squandering it on far-flung acquisitions with tenuous ties to the core business.

This all raises the question of what anyone can do to compete with that.

The U.S. government is fully aware of the state of Taiwan's currency and has steadily declined to take any action against it. Competing in foundry requires outside funding pools. For Intel, that has led to further calls for direct government support.

We would obviously prefer a more commercial solution, in the form of investment from prospective customers, but there is a rising chorus begging encouraging the U.S. government to "save" Intel by subsidizing some group of equity holders.

The less obvious question is how Samsung can respond. The South Korean Won's status is actually not far off from the NT$, for similar reasons, but Samsung has chosen to spend that windfall elsewhere.

In the short run, Samsung Foundry will likely need support from the broader Samsung Chaebol. It's unclear to us to what degree the chaebol is interested in propping up Foundry. The memory business is important for the whole group. Does Foundry put that at risk? Does the cash burn from Foundry get so large that eventually the chaebol decides to fall back and focus on memory?

What is clear is that both Intel and Samsung will need considerable outside support to stay in the game.

Intel vs. TSMC: Why economic factors, not tech, are at the heart of America's chip struggle