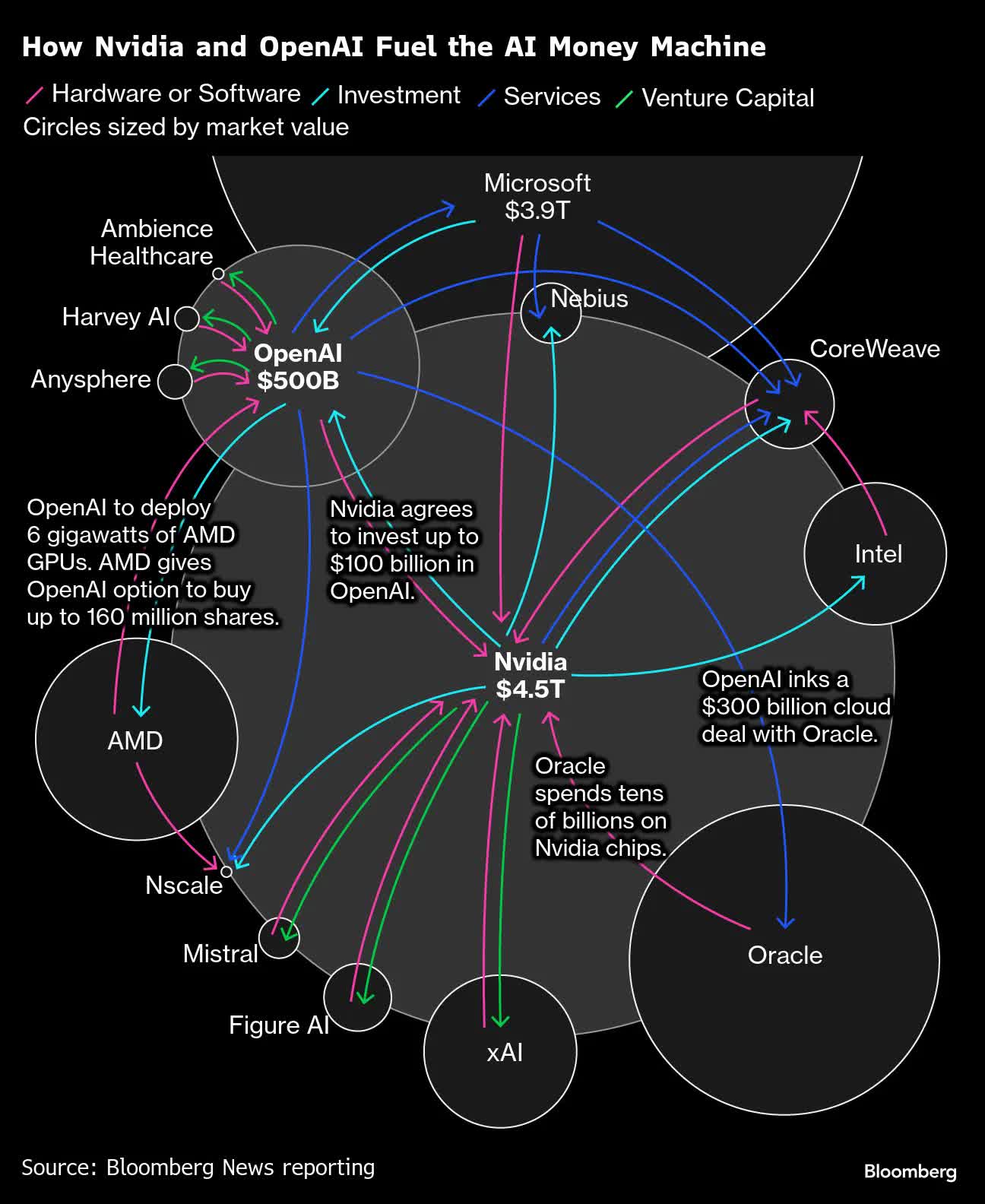

Bottom line: Nvidia's explosive rise to become the world's most valuable company has come with an uneasy question from investors: how much of its record-breaking growth depends on financing its own customers? Now worth more than $4 trillion, Nvidia designs the specialized silicon and software that power AI systems, from data centers hosting ChatGPT to national AI computing hubs. But behind that scale lies a complicated web of investments that critics say resembles vendor financing – a practice in which a company lends money to customers who use those funds to buy its products.

The concern centers on circular financial flows between Nvidia and companies that depend heavily on its chips. Nvidia has committed to invest $10 billion annually in OpenAI for the next decade, most of which will fund purchases of its own hardware. It has also arranged deals with CoreWeave, an AI cloud provider that essentially resells or leases access to Nvidia's chips, while receiving Nvidia's financial backing in parallel.

Comparisons have surfaced with Lucent Technologies, the former telecom supplier that collapsed after using similar arrangements to drive sales in the late 1990s. Nvidia has firmly rejected any equivalence. In a leaked memo, the company said it "does not rely on vendor financing arrangements to grow revenue."

Source: Bloomberg

Still, skepticism persists among long-term investors. James Anderson, a prominent technology investor, told The Guardian this year that the OpenAI deal presented "more reason to be concerned there than before." He added, "I have to say the words 'vendor financing' do not carry nice reflections to somebody of my age. It's not quite like what many of the telecom suppliers were up to in 1999 – 2000, but it has certain rhymes to it. I don't think it makes me feel entirely comfortable from that point of view."

The scale of the commitments underpinning the AI ecosystem is immense. OpenAI alone has staked around $1.4 trillion on computing power, much of it built on Nvidia infrastructure. It argues that Nvidia's and AMD's investment ties are meant to align incentives and accelerate deployment rather than create dependence. CoreWeave's chief executive, Michael Intrator, has described the structure as a pragmatic response to "a violent change in supply and demand."

Industry analysts caution that Nvidia's exposure may reflect the broader economics of artificial intelligence rather than accounting manipulation, as its financial future depends in large part on whether AI adoption continues fast enough for customers such as OpenAI, Anthropic, and CoreWeave to remain solvent...

Beyond these arrangements, Nvidia has deployed special-purpose vehicles, or SPVs, to structure investments – including a $2 billion fund tied to Elon Musk's xAI, whose proceeds are earmarked for chip purchases.

The mechanism has drawn comparisons with Enron, which used SPVs to obscure debt and inflate earnings before collapsing in 2001. Nvidia has rejected any similarity, asserting that its reporting is "complete and transparent" and that it "does not use special-purpose entities to hide debt and inflate revenue."

Industry analysts caution that Nvidia's exposure may reflect the broader economics of artificial intelligence rather than accounting manipulation, as its financial future depends in large part on whether AI adoption continues fast enough for customers such as OpenAI, Anthropic, and CoreWeave to remain solvent. If revenues falter, Nvidia could face write-downs on those equity stakes and unpaid receivables.

The chipmaker has also inked high-value but opaque agreements with governments, including South Korea and Saudi Arabia, committed to deploying hundreds of thousands of Nvidia's Blackwell chips.

The company disclosed some details, such as the estimated 260,000 chips going to South Korean buyers, but not deal values. Saudi Arabia's state-backed AI startup Humain has announced plans to buy up to 600,000 chips, without clear timing or pricing.

The company's CFO, Colette Kress, told investors in December that Nvidia does not see an AI bubble and predicted trillions of dollars of potential business over the next decade. For now, markets appear to be in agreement. But the underlying structures that helped propel Nvidia's trillion-dollar ascent may yet test whether its success rests on solid ground – or on the same circular financing patterns that haunted earlier eras of tech history.

Nvidia's $4 trillion rise raises questions about financing its own customers