Bottom line: A key measure of credit risk linked to Oracle has climbed to its highest level in three years, and Wall Street analysts warn that pressure is likely to intensify next year unless the company does more to explain how it will fund its artificial intelligence expansion. The shift reflects mounting anxiety over the scale, structure, and timing of Oracle's borrowing as it races to add data center capacity for AI workloads.

Morgan Stanley credit analysts Lindsay Tyler and David Hamburger describe several fault lines: a growing gap between spending and available funding, a balance sheet that continues to swell, and the possibility that assets built for today's AI architectures could become outdated faster than expected. They argue that these issues are now being priced directly into the cost of default protection on Oracle's debt.

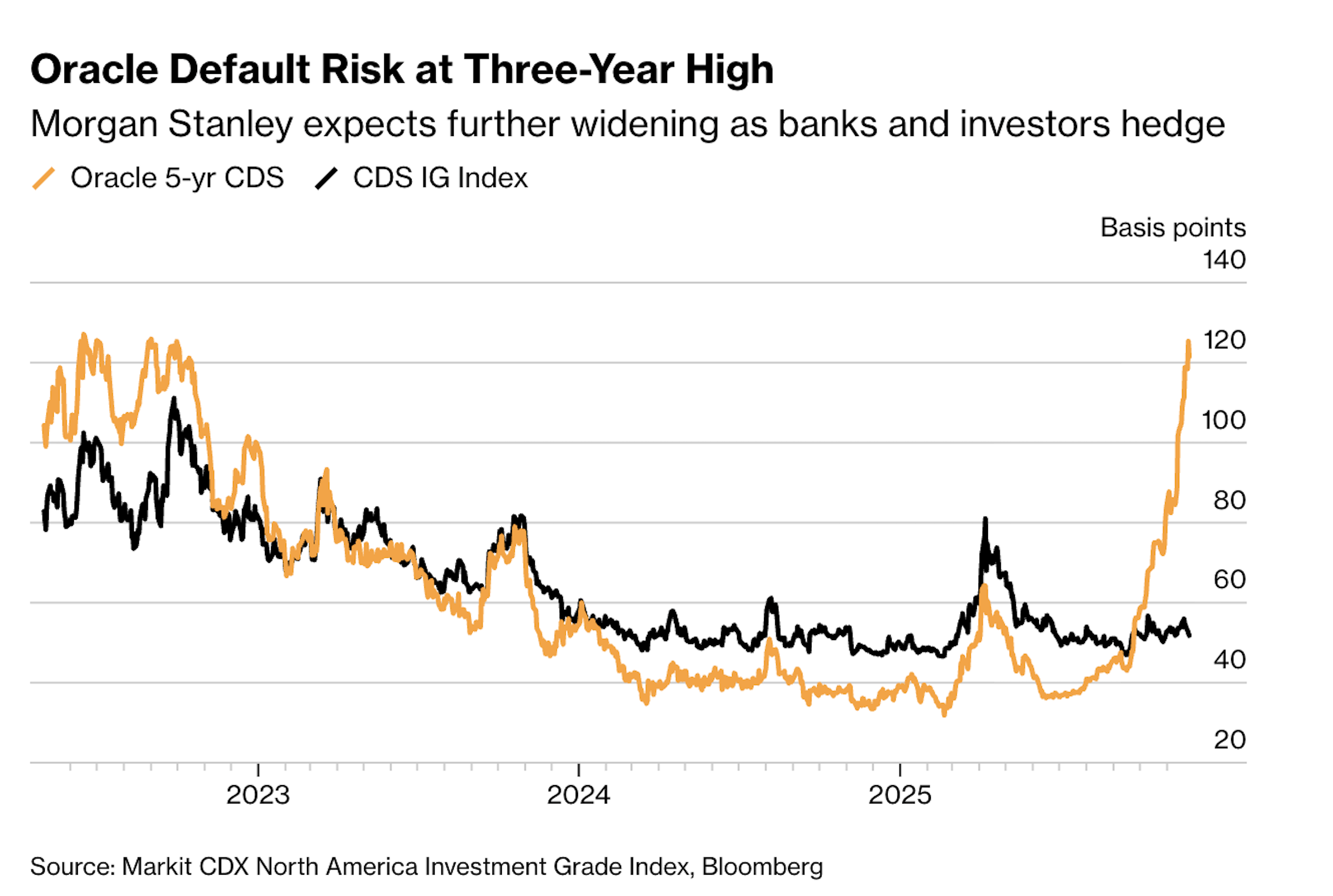

The cost of five-year credit default swaps on Oracle rose to 1.25 percentage points a year in late November, according to ICE Data Services, marking the highest level since 2022. That means buyers of protection are paying 125 basis points annually to insure against a default over five years, a sharp step-up from earlier in the AI cycle. The swaps are now close enough to crisis-era territory that analysts are openly discussing whether the all-time peak set in 2008 could be challenged.

In their note, Tyler and Hamburger say Oracle's five-year CDS spread could break above 1.5 percentage points in the near term and might move toward two percentage points if the company continues to provide only limited detail about its financing strategy as 2026 approaches.

Credit: Bloomberg

For reference, Oracle's default swaps hit a record 1.98 percentage points during the 2008 financial crisis. Oracle declined to comment on the assessment or the recent trading in its credit protection.

Oracle has become one of the main corporate symbols of AI-related credit risk because it relies heavily on debt markets to support its infrastructure plans. In September, the company raised $18 billion in the US investment-grade bond market, adding a large new slug of conventional corporate debt to its capital structure.

Weeks later, a syndicate of roughly 20 banks arranged an additional $18 billion project finance loan to build a major data center campus in New Mexico, with Oracle set to step in as the tenant once the facilities are completed.

On top of that, banks are assembling a separate $38 billion loan package to back the construction of data centers in Texas and Wisconsin being developed by Vantage Data Centers, where Oracle is expected to be the anchor tenant.

Credit: App Economy Insights

Over the past two months, Tyler and Hamburger say it has become clearer that these construction loans, rather than Oracle's traditional bond financing alone, are a major driver of hedging flows. The analysts also note that some of this hedging might unwind if and when the originating banks distribute pieces of the loans to other investors, though they stress that new holders may then choose to hedge as well.

The result is an environment in which both banks and bondholders use Oracle's CDS as a flexible tool to manage exposure to AI-linked credit risk. Morgan Stanley previously argued that near-term credit deterioration and uncertainty would fuel further hedging among traditional bond investors, direct lenders, and "thematic" players who want a macro way to trade the AI spending boom.

In their latest comments, the analysts say both the bondholder and thematic hedging dynamics could become more critical over time as the market internalizes the scale of Oracle's commitments.

This has had visible consequences in performance metrics. Oracle's CDS spreads have widened more than those of the broader investment-grade CDX index, indicating that investors are demanding a higher premium to insure Oracle than for the average high-grade borrower. At the same time, Oracle's cash bonds have lagged the Bloomberg high-grade corporate index, reflecting weaker demand for its debt amid hedging activity and heightened concerns about leverage.

The Morgan Stanley team has also changed its recommended trading stance. Earlier this year, the bank had favored a "basis trade" that involved buying Oracle bonds and simultaneously buying CDS protection, on the view that the derivative spreads would widen more than the underlying bond spreads.

Now, the analysts are abandoning the bond leg of that strategy. They maintain that an outright CDS trade is cleaner in the current environment and more likely to benefit from further spread widening if concerns about Oracle's funding plans, balance sheet trajectory, and AI spending persist. For investors, that recommendation underscores how a company at the center of the AI race has also become a preferred vehicle for expressing caution about the financial risks of that race.

Oracle's credit risk is spiking as Wall Street asks how it's going to pay for all that AI

{kind=link}