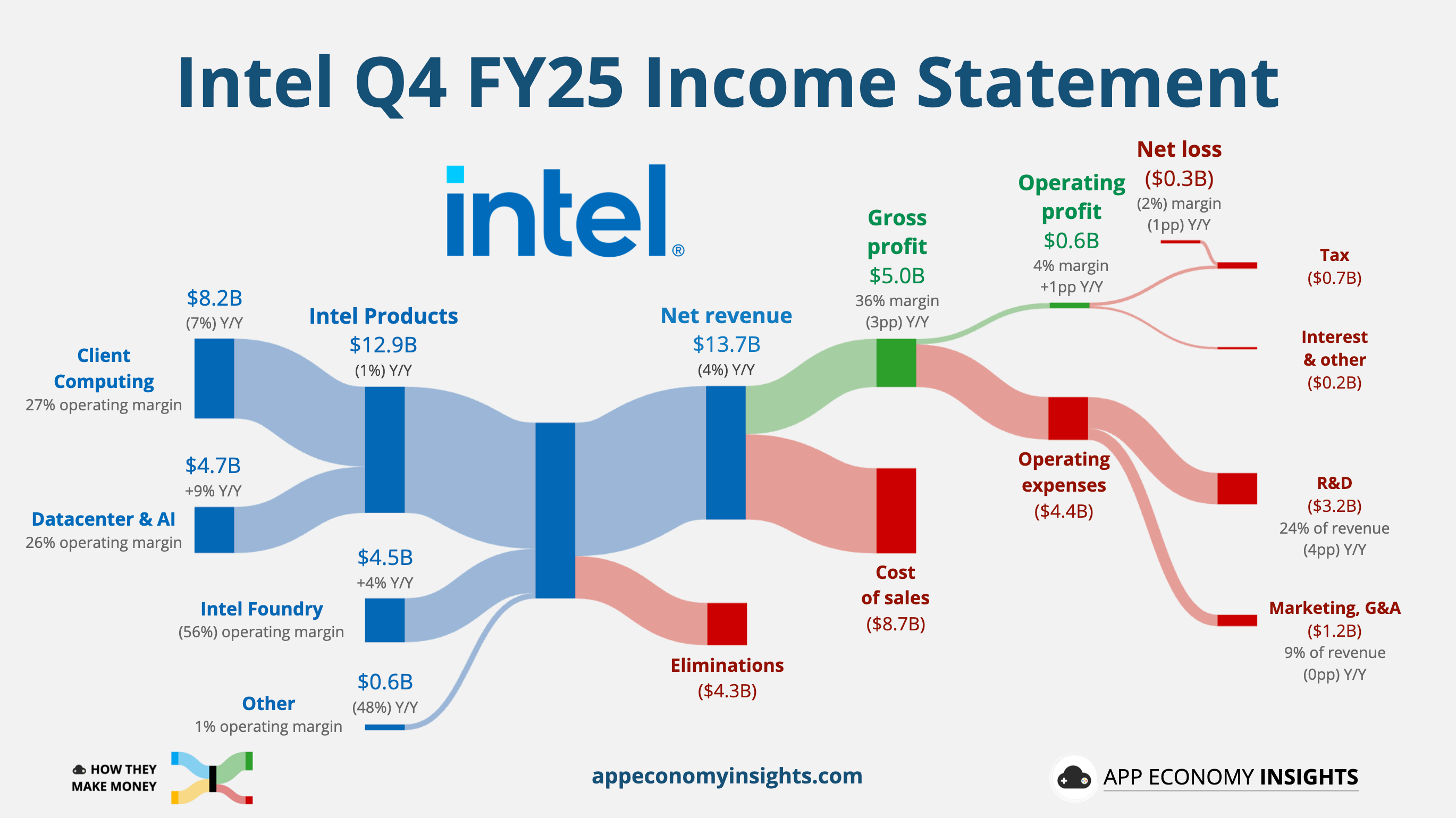

Intel's fourth-quarter results reflected rising demand for its AI and data center products, offset by persistent supply constraints that continue to pressure its consumer segment. The semiconductor giant reported $13.7 billion in revenue for Q4 2025, down 4 percent year over year but near the high end of its guidance. Annual revenue fell slightly, from $53.1 billion to $52.9 billion.

The mixed results highlight a fundamental tension within Intel's business: the company is selling nearly every chip it produces, yet still can't keep up with demand. Supply shortfalls have forced executives to prioritize high-margin segments while rationing production of consumer processors.

Intel's data center and AI division was a standout performer, posting quarterly revenue growth of nine percent and annual growth of five percent. Gains came as cloud providers and enterprise customers increased demand for new Xeon and AI accelerator lines optimized for massively parallel workloads. In contrast, Intel's client computing group – responsible for Core processors, Arc graphics, and other personal computing products – saw revenue decline seven percent for the quarter and three percent for the year.

Credit: App Economy Insights

The imbalance has led management to shift manufacturing priorities toward the business segment, generating stronger margins. Chief Financial Officer David Zinsner said Intel is focusing its internal wafer supply on data center products while outsourcing a larger portion of consumer chip production to external foundries such as TSMC.

That prioritization could lead to potential shortages or pricing pressure for Intel's upcoming consumer lineup, including the new Core Ultra Series 3 processors, codenamed Panther Lake. Unlike their predecessors, which relied heavily on TSMC fabrication, these chips are being produced mostly in-house.

Zinsner acknowledged that Intel cannot fully abandon the client market, but the company is shifting as much production as possible toward data center products. The decision reflects where demand is strongest and most profitable at a time when every usable wafer counts.

Intel's production problems stem largely from its 18A node, the advanced chipmaking process intended to help the company regain technological leadership. The transition has been uneven, with yield rates below expectations. Intel says yields are improving by seven to eight percent each month, but those gains come from a low baseline, as reports from mid-2025 indicated that only about 10 percent of early 18A wafers met quality thresholds.

While CEO Lip-Bu Tan described current yields as "in line with internal plans," he acknowledged they remain below desired levels. Both Tan and Zinsner indicated that output should recover in the second quarter of 2026, with the first quarter representing the "trough" of supply constraints.

Intel is simultaneously preparing its next fabrication nodes and architectural overhauls. Work continues on the refined 18A process and its successor, 14A, which could allow Intel's foundries to serve third-party customers for the first time in decades. The company expects to begin securing commitments from external partners between late 2026 and early 2027, shaping future capacity planning.

On the design front, Intel plans to release its next-generation Nova Lake architecture at the end of 2026. The platform will unify Intel's desktop and laptop processor families and use the 18A process for at least part of its production.

Despite supply challenges, Intel demonstrated resilience in Q4, driven by strong demand for AI and data center products. The company now faces the dual task of ramping production to meet consumer needs while preparing its next-generation nodes and architectures, setting the stage for growth in 2026 and beyond.