Rich Wafers: Foundry corporations have become the cornerstone of today's computing industry. They can etch and manufacture the complex chip blueprints Nvidia and other Big Tech players develop in their labs, and are making a massive amount of money as a result.

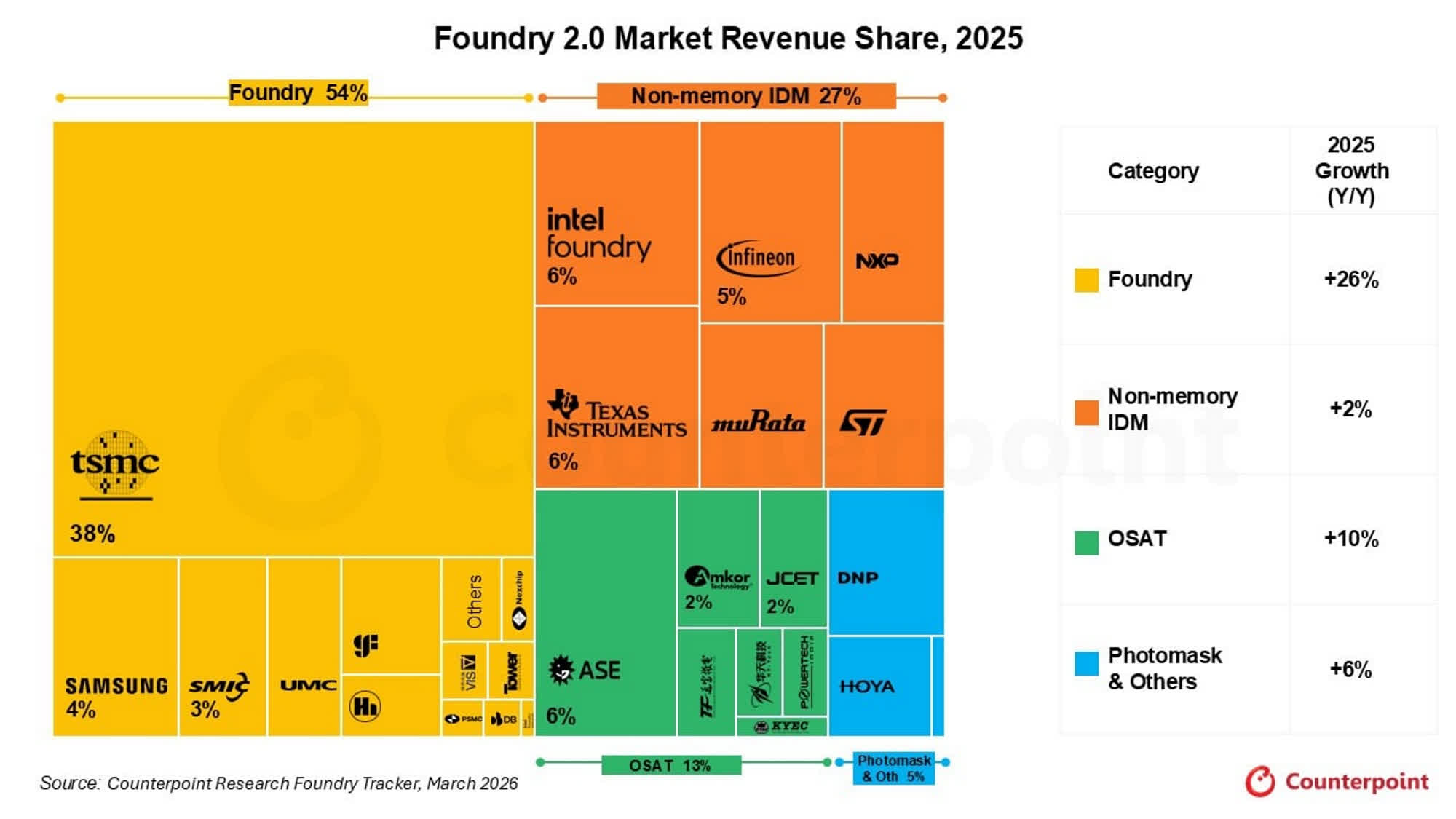

A new report by Counterpoint Research highlights the business results of the extremely successful players in the foundry business. The research company coined the "Foundry 2.0" term because today's landscape is apparently much more complex and multifaceted than the traditional chip-making business. Either way, most silicon manufacturers have become massively rich, with TSMC the richest of them all.

The newly released Global Foundry 2.0 study states that semiconductor manufacturers collected $320 billion in revenue during 2025. The market grew by 16% year-over-year, and everyone knows why: AI chips. The "sustained," ever-growing demand for AI accelerators pushed the market to new heights, with advanced packaging processes doing their part.

TSMC confirmed its role as the world's largest pure foundry player, growing by a massive 36% year-over-year in 2025. The Taiwanese conglomerate makes chips for some of the largest tech firms in the world, and is now suffering from significant, prolonged capacity constraints because customers keep asking for more.

TSMC's results aside, other pure foundry players experienced a more modest 8% grow in 2025. Chinese vendors achieved the best results, thanks to an increase in their domestic localization efforts.

Counterpoint's report also highlights the good results achieved by Outsourced Semiconductor Assembly and Test (OSAT) players, whose revenue grew by 10% year-over-year. OSAT companies are now absorbing the spillover demand that TSMC cannot meet anymore, testing newly developed silicon solutions designed for AI workloads.

Samsung, the second-largest foundry company after TSMC, experienced a mixed year. However, Counterpoint expects the Korean giant to significantly improve in 2026 thanks to its diversification efforts. The company has already acquired high-value designs, and demand for its 4nm manufacturing node can be described as "solid." Chinese foundries such as SMIC (16%) and Nexchip (24%) experienced double-digit growth, and they're expected to keep growing in 2026.

OSAT and other non-pure foundry ventures will likely play a key role in providing packaging solutions such as CoWoS-S and CoWoS-L. Advanced packaging is expected to grow by 80% in 2026, Counterpoint said. Customers are now looking to integrate different computing elements such as CPUs, GPUs, and custom ASICs into the same computing system.

Counterpoint said that the new Foundry 2.0 model "reflects a gradual shift away from the traditional pure-play model toward a more integrated ecosystem. In practice, this means closer alignment across design, manufacturing, and packaging, ultimately improving system-level efficiency and total cost of ownership (TCO)."