Why it matters: According to Trendforce, Taiwan will control 48% of the global foundry capacity in 2022, making it the undisputed leader. Even with the increasing number of countries trying to bring semiconductor production within their borders, it's expected that this figure will only drop to 44% by 2025.

Following the past few years of chip shortages caused by pandemic shutdowns and geopolitical turmoil, more and more governments are trying to create local chip production industries. Many of them are turning to Taiwanese companies to help them set up their factories.

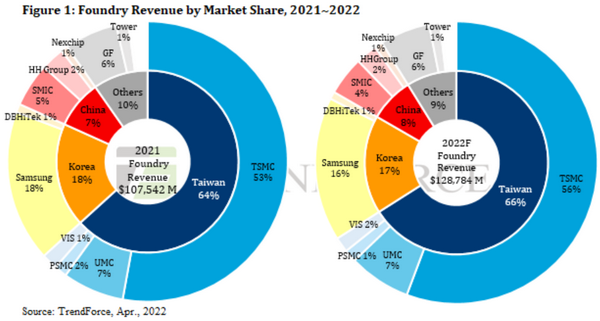

This is because Taiwan is crucial to the global semiconductor supply chain, accounting for a 26% market share of the total semiconductor revenue in 2021, ranking it second worldwide. The country commands a 27% and 20% market share in the IC design and the packaging and testing industries, respectively. It also accounts for a staggering 64% of the worldwide foundry revenue.

TSMC currently possesses the most advanced process technology, and it plans to keep most of the production of future N3 and N2 nodes in Taiwan. Meanwhile, other Taiwanese foundries like UMC, Vanguard, and PSMC cover applications that don't require bleeding-edge nodes, such as automotive and IoT.

Currently, Taiwan has the most 8-inch and 12-inch fabs, 24 of them, followed by China, South Korea, and the US. As far as future foundries go, Taiwan still tops the list with six, followed by China with four, while the US plans to build three new fabs.

Even so, Trendforce expects that Taiwan will still control 44% of the world's foundry capacity by 2025 and as much as 58% of the worldwide capacity for advanced processes (16 nm and below).