Bottom line: While Nvidia's soaring revenues continue to command attention, its heavy reliance on a small group of clients introduces both opportunity and uncertainty. Market observers remain watchful for greater clarity around customer composition and future cloud spending, as these factors increasingly shape forecasts for the chipmaker's next phase of growth.

A new financial filing from Nvidia revealed that just two customers were responsible for 39 percent of the company's revenue during its July quarter – a concentration that is drawing renewed scrutiny from analysts and investors alike. According to documents submitted to the Securities and Exchange Commission, "Customer A" accounted for 23 percent of Nvidia's total revenue, while "Customer B" represented 16 percent.

This level of revenue concentration is significantly higher than in the same period one year ago, when Nvidia's top two customers contributed 14 percent and 11 percent, respectively.

Nvidia routinely discloses its leading customers on a quarterly basis. However, these latest numbers have prompted a fresh discussion about whether Nvidia's growth trajectory is heavily dependent on a small group of enormous buyers, particularly large cloud service providers.

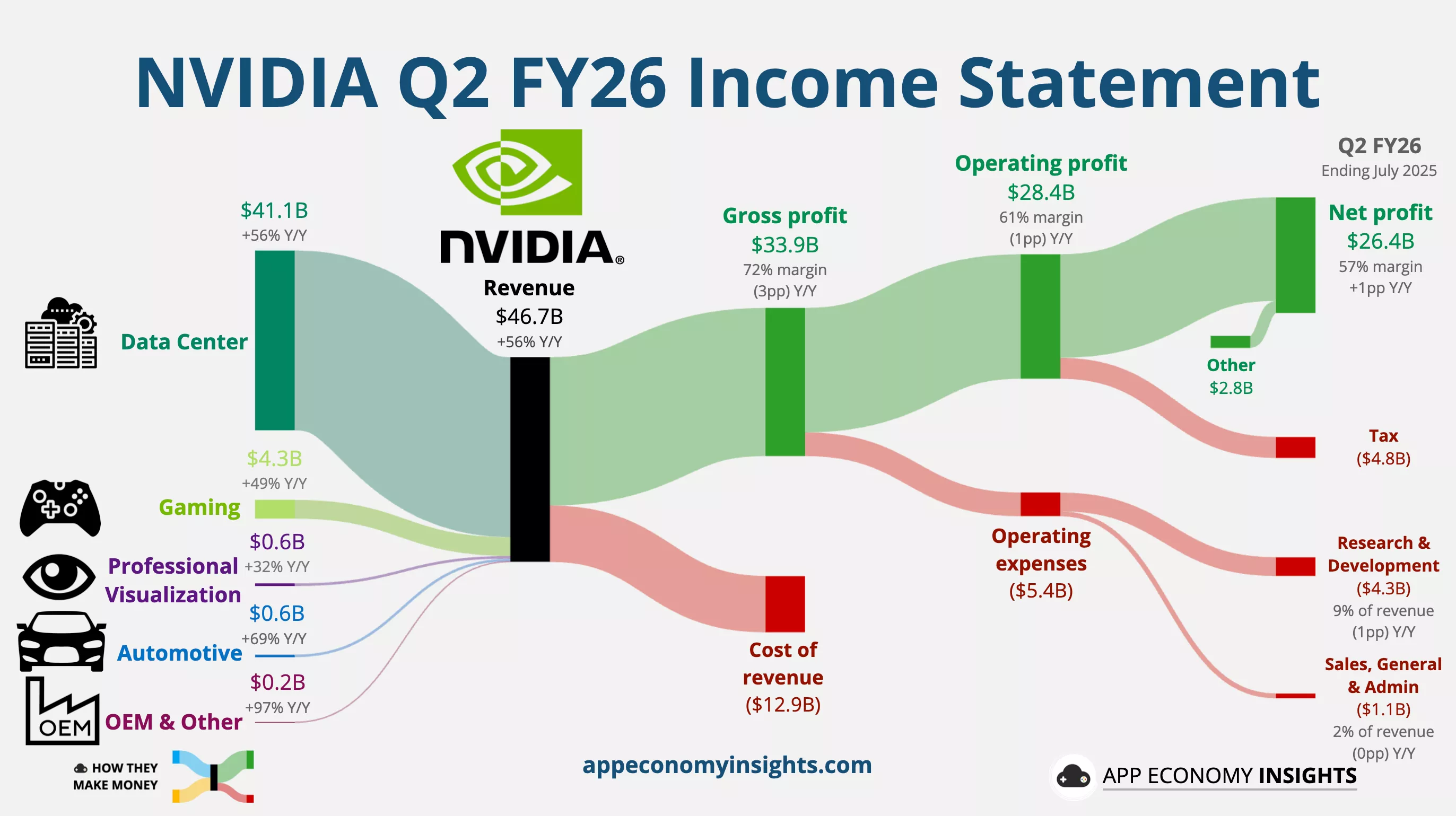

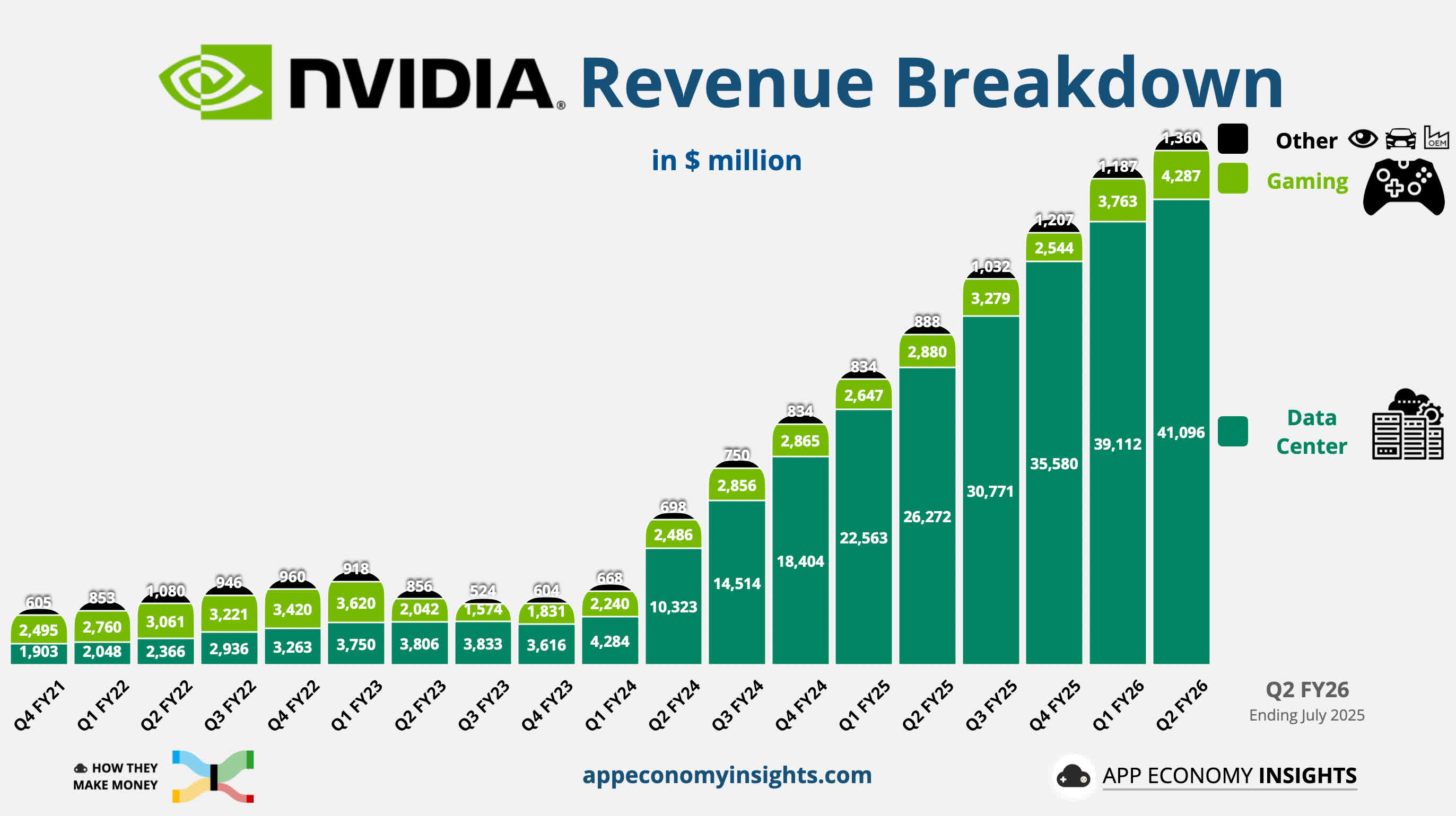

Graphs by App Economy Insights

Speculation is circulating that big tech and cloud giants such as Microsoft, Meta, Amazon, Google, and Oracle may be among Nvidia's highest spending customers. However, despite the increased focus, Nvidia has declined to identify the customers cited in its filing, and their identities remain unclear.

The company's definitions for direct and indirect customers add further complexity. Nvidia defines direct customers as companies that buy its chips to manufacture complete systems or circuit boards. These are then resold to data centers, cloud providers, and end-users. Direct customers might include system integrators, distributors, or original equipment manufacturers such as Foxconn or Quanta.

Indirect customers include cloud service providers, internet companies, and enterprises, who often purchase through Nvidia's direct customers.

The company acknowledged in its filing that it may continue to derive significant revenue from a limited number of buyers: "We have experienced periods where we receive a significant amount of our revenue from a limited number of customers, and this trend may continue," Nvidia wrote.

The mystery surrounding the identity of Customer A and Customer B has implications for investors and industry watchers, who increasingly rely on cloud capital expenditure data to predict Nvidia's growth.

Some analysts, such as HSBC's Frank Lee, have expressed caution. "We see limited room for further earnings upside revision or share price catalyst in the near-term unless we have increasing clarity over upside in 2026 [cloud service provider] capex expectations," Lee said in a recent note.

Adding to the uncertainty, Nvidia disclosed that two indirect customers – primarily buying systems through Customers A and B – each contributed more than 10 percent of total company revenue in the quarter. The company also reported that an "AI research and development company" provided a "meaningful" amount of revenue through both direct and indirect channels.

Nvidia's leadership emphasized that demand for AI systems remains strong across a wide range of customer types, including enterprises and "neoclouds," entities aiming to rival established cloud providers with AI-focused services.

The company also highlighted contributions from foreign governments, noting it expects up to $20 billion in annual revenue from "sovereign AI" initiatives.

As the AI market expands, Nvidia is forecasting significant growth in infrastructure investment. CEO Jensen Huang presented a new estimate for AI infrastructure spending, projecting a total market size of $3 to $4 trillion by 2030. He also noted that Nvidia could capture approximately 70 percent of the total cost of a $50 billion AI-focused data center, including both graphics processing units and other specialized chips. "As you know, the capex of just the top four hyperscalers has doubled in two years as the AI revolution went into full steam," Huang said.

Nearly 40% of Nvidia's revenue tied to two mystery customers, filing shows

{kind=link}