In a nutshell: The global server market reportedly reached a record $95.2 billion in value during the first quarter of this year and is projected to hit $366 billion by the end of calendar year 2025. A key driver of this growth is the rise of Arm-based servers, which are expanding at nearly 70 percent year-over-year and accounted for 21.1 percent of total server shipments in Q1 2025.

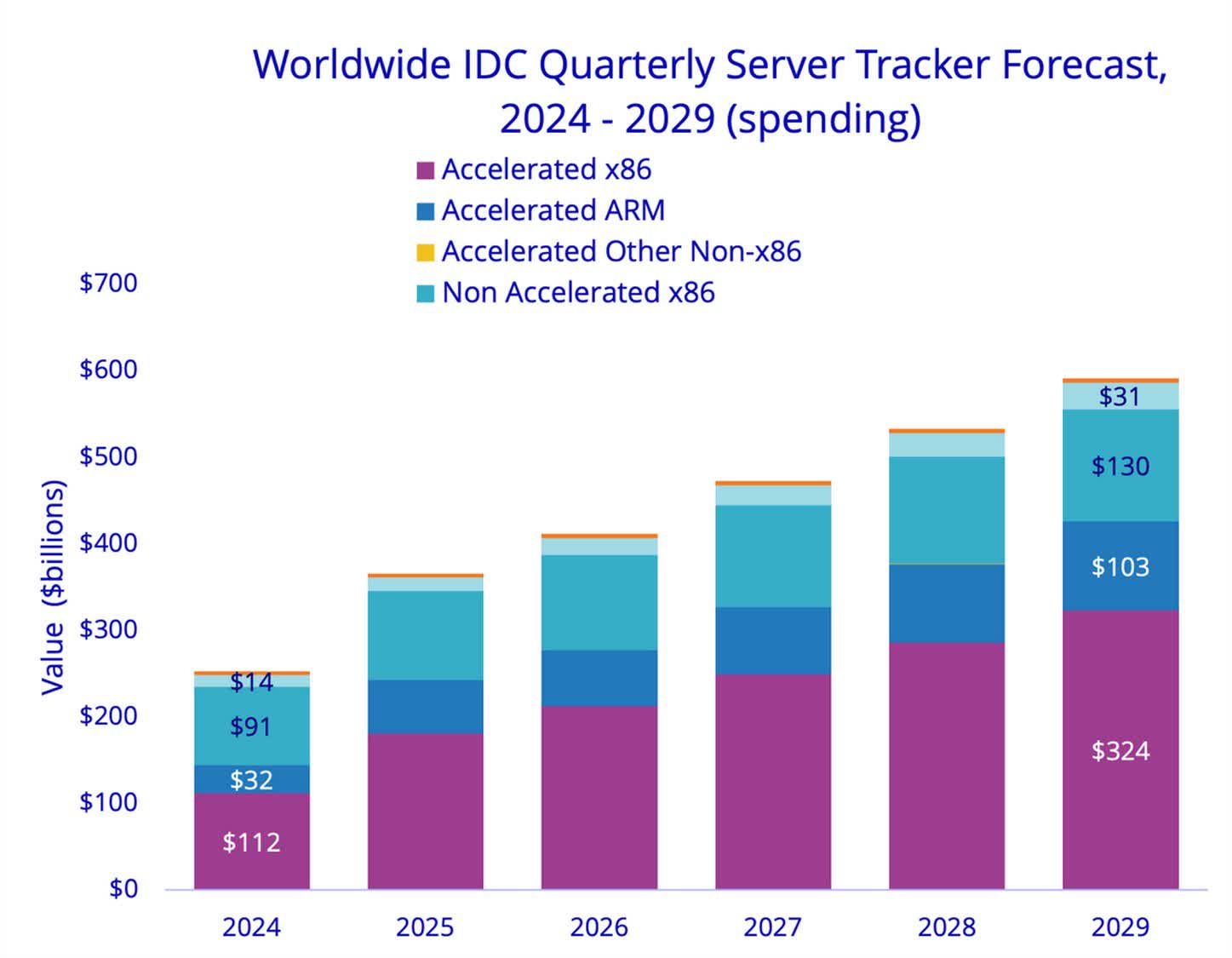

According to the latest data from IDC, the global server market grew by 134 percent year-over-year in Q1 2025, driven by a sharp increase in the deployment of GPU-embedded systems, which are essential for AI inferencing and training workloads. This segment is projected to grow at an annual rate of 46.7 percent and by the end of the year, it is expected to account for nearly 50 percent of the server market by value.

The report also notes that the GPU-embedded server segment has tripled over the past three years, fueled by continued investments from hyperscalers and cloud service providers.

The data additionally suggests that Arm-based servers are continuing to erode x86's market dominance, growing 39.9 percent year-over-year, with shipments expected to reach $283.9 billion in 2025. Non-x86 servers overall are projected to grow by 63.7 percent this year, hitting $82 billion. The surge is largely driven by high-density, rack-scale configurations designed for compute-heavy AI workloads.

The US remains at the forefront of this growth, accounting for approximately 62 percent of all server market revenue. Server shipments in the US are forecasted to grow by 59.7 percent year-over-year in 2025. China's server market is also expanding rapidly, with a projected 39.5 percent year-over-year growth for the same period.

Elsewhere, Japan, Asia, Europe, the Middle East, and Latin America are expected to grow between 10.8 percent and 33.9 percent in 2025. Canada is the only major market projected to contract, with a 9.6 percent decline attributed to what IDC describes as "an outsized acquisition in 2024 that skewed the comparative baseline."

Even as the global server market reaches new highs, Intel continues to face mounting pressure from both a resurgent AMD and the rapid rise of Arm. As of June 2025, data shows AMD holds roughly 33 percent of the server CPU market, while accounting for over 50 percent of total revenue.

BofA) AI Servers – Compute (CPU, GPU, ASIC, XPU) 1

– Jukan Choi (@Jukanlosreve) June 26, 2025

An AI server refers to the most basic single computer configuration, typically consisting of a CPU, an accelerator (GPU, ASIC, or XPU), and associated memory.

CPU

Every server requires a CPU. Over time, the value contribution… pic.twitter.com/TLvCKVKRSl

The report further confirms that AMD is dominating the premium server CPU segment with its latest Epyc processors, while Intel retains a strong presence in the budget segment through its Xeon Scalable offerings.

Once commanding nearly 100 percent of the server CPU market, Intel's share has now dropped to around 62 percent. Due to delays in launching its Sapphire Rapids platform, Intel's market share is expected to fall further to 55 percent by the end of 2025, while AMD is projected to climb to 36 percent.

Looking ahead, Intel's share could dip below 50 percent by 2027, with AMD reaching approximately 40 percent of global server CPU revenues. By 2028, the two companies are expected to generate roughly equal revenue in the server CPU space.

Meanwhile, Arm is poised to continue its rapid ascent, with projections suggesting it could capture 10 – 12 percent of global server CPU revenue within the next two to three years.