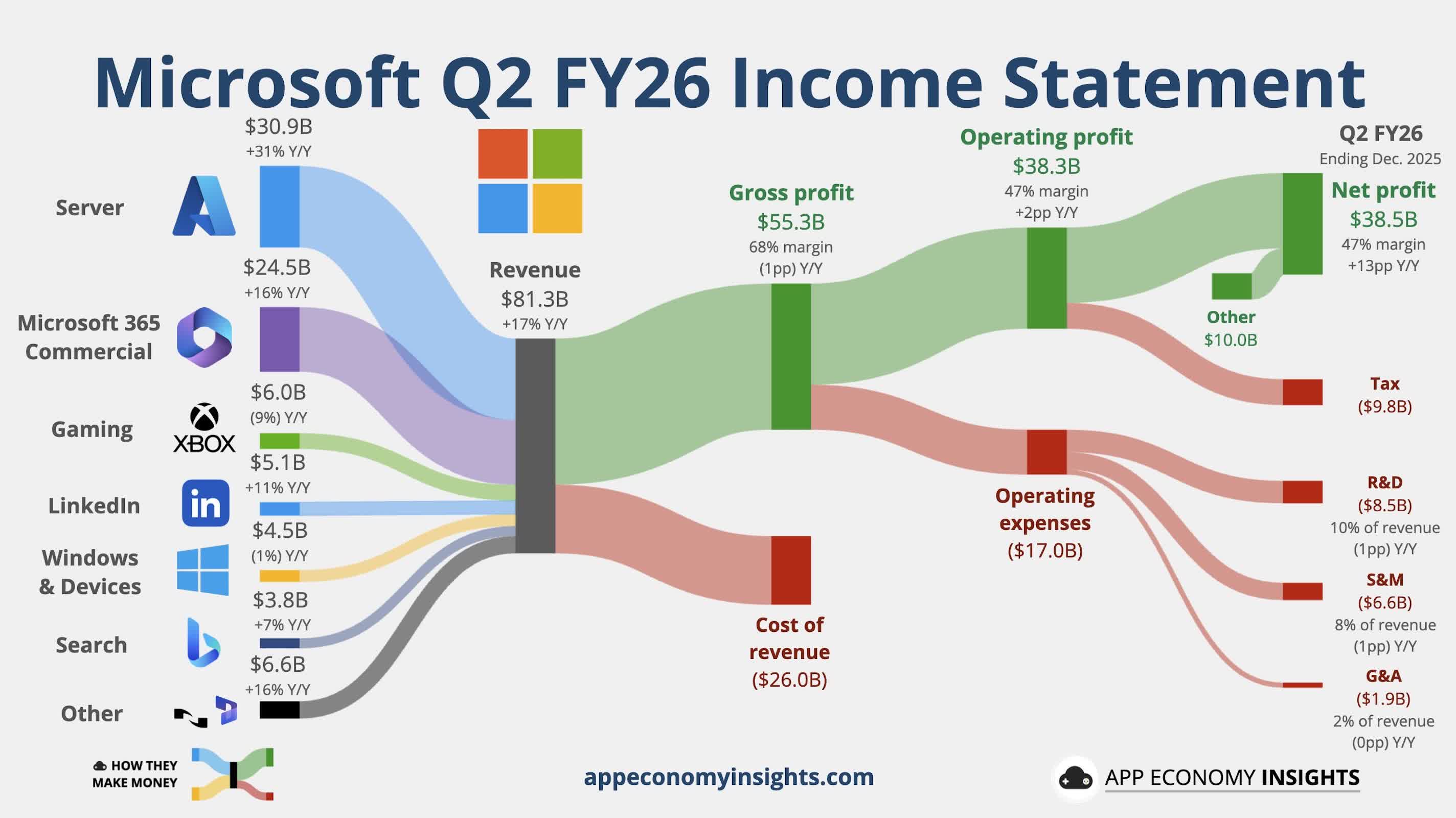

In context: Microsoft reported another strong quarter, with revenue rising 17 percent to $81.3 billion and net income increasing 21 percent to $38.3 billion. The company also reached a symbolic milestone: its cloud business generated more than $50 billion in a single quarter, the highest in its history. Yet despite these headline numbers, the market responded coolly. Shares fell on Thursday as analysts questioned whether the company's escalating spending on AI infrastructure might be stretching resources too far, too fast.

The concern stems from Microsoft's capital expenditures, which have soared to near-record levels. The company spent $88.2 billion last fiscal year and $72.4 billion in the first half of the current fiscal year.

Most of this spending is aimed at building new data centers and high-performance computing infrastructure to support AI workloads for enterprises and major research partners, including OpenAI and Anthropic. The strategy is clear: saturate the market with capacity before demand peaks. What remains uncertain is how quickly that demand will convert into sustained profits.

Wall Street's ambivalence reflects growth in Microsoft's core platforms. Azure, the company's enterprise cloud division, and Microsoft 365, its productivity suite, both posted solid but slightly slower expansion than investors had anticipated.

UBS analyst Karl Keirstead described the underperformance as the key factor weighing on sentiment, though he still rated the stock a buy. The slower growth doesn't signal weakness – overall expansion remains strong – but it contrasts with Microsoft's image as the primary beneficiary of the AI boom.

During the earnings call, CEO Satya Nadella sought to reframe the narrative, spending considerable time explaining how Microsoft's AI initiatives are driving user engagement.

Nadella said adoption of Copilot, Microsoft's flagship consumer AI assistant, has nearly tripled in daily usage compared to a year ago. He did not disclose exact user numbers but highlighted its integration across Microsoft's ecosystem – from search and news feeds to the Windows operating system. The company's last publicly reported figure was 100 million monthly active users across both consumer and business segments.

Turns out if you rename all of your products to CoPilot then people use CoPilot a lot.

– JD (@Dizz_012) January 29, 2026

More concrete details were provided for GitHub Copilot, Microsoft's AI coding assistant. The service now has 4.7 million paid subscribers, a 75 percent year-over-year increase. Including free users, GitHub reported a total Copilot user base of 20 million last year, making it one of the most widely adopted developer AI tools to date.

Meanwhile, Microsoft 365 Copilot has secured 15 million paid enterprise seats – a fraction of its 450 million total business customers – but a sign that corporate adoption is accelerating.

Nadella also highlighted a quieter success story in Microsoft's healthcare division. Dragon Copilot, the company's AI agent for medical professionals, now serves 100,000 providers and processed 21 million patient encounters this quarter, tripling usage from a year ago.

The product competes in a rapidly growing space that includes startups such as Harvey and reflects Microsoft's strategy to expand AI into specialized verticals beyond its core enterprise base.

Behind these metrics lies the rationale for Microsoft's enormous capital push. Both Nadella and CFO Amy Hood noted that AI demand is already exceeding current data center capacity, leaving new compute infrastructure effectively booked the moment it comes online.

The implication is that Microsoft's data center expansion is not speculative spending but a response to existing utilization. That framing may reassure investors, though the numbers suggest that even "booked to capacity" could involve billions in sunk costs before operating margins catch up.

For now, Microsoft's results illustrate a company redefining scale in the cloud era. Market skepticism may fade if its data infrastructure gamble translates into consistent AI-driven revenue across its portfolio. But with capital spending already approaching last year's record, and only halfway through the fiscal year, Microsoft is betting heavily that global demand for AI compute will grow faster than even its vast supply capacity.