Bottom line: Demand for AI infrastructure has been reshaping how investors value chipmakers, and recent results from key suppliers have strengthened the view that compute-intensive workloads will continue to grow. The effect has been evident with CPU vendors as of late. AMD's stock traded at $278 on Thursday, putting its market value at about $454 billion. Intel's rally from early March pushed the stock toward $68 and lifted its market cap to just under $340 billion. Arm's shares, meanwhile, traded close to $165, valuing the company at roughly $174 billion.

Those gains point to a broader realignment toward infrastructure built for emerging AI workloads, particularly agentic systems and retrieval augmented generation. Both lean heavily on sustained compute performance and memory throughput, putting renewed weight on CPU design, especially in systems where orchestration, preprocessing, and data movement remain CPU-bound even when GPUs handle the bulk of training and inference.

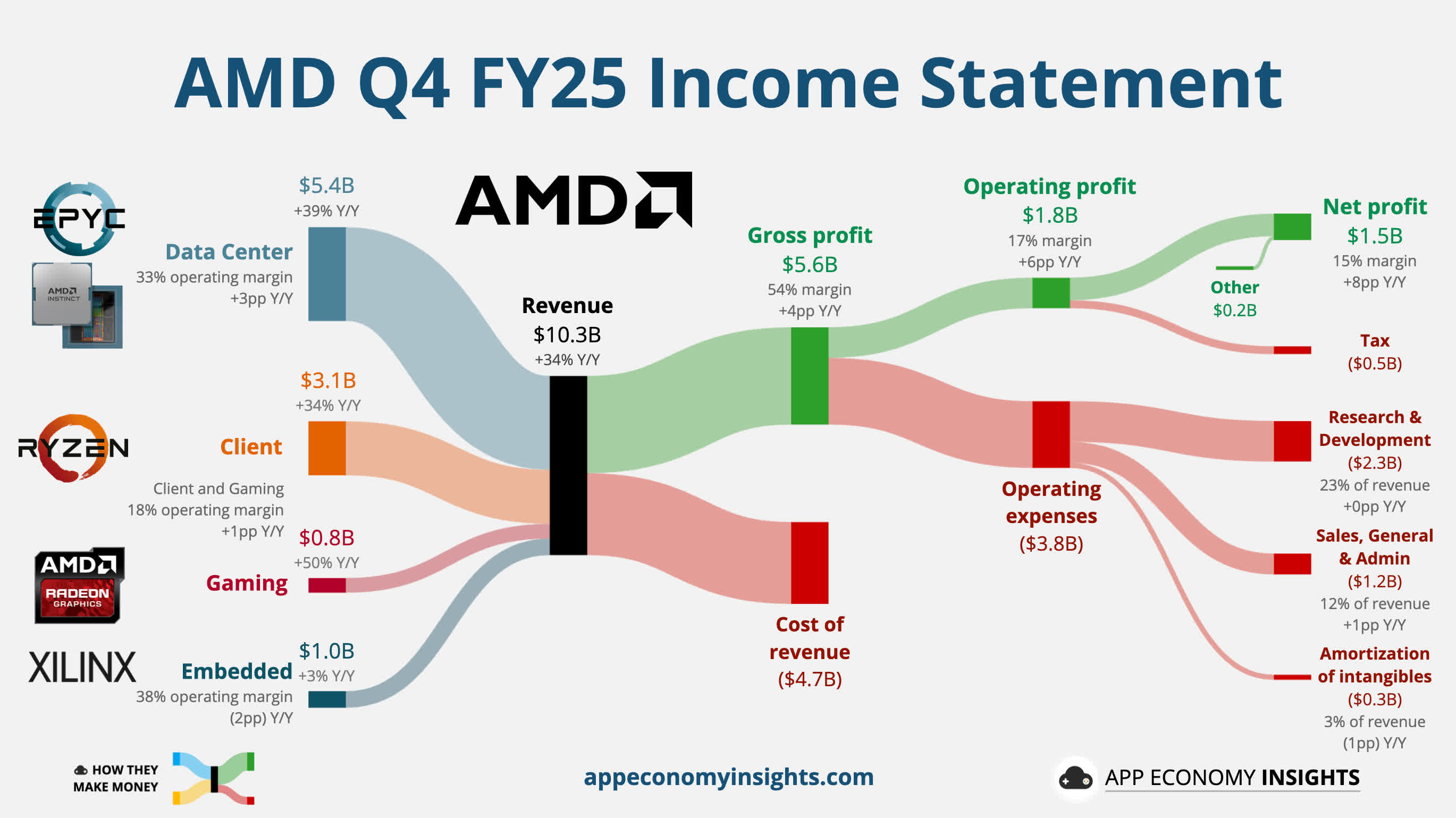

That dynamic is becoming central to how investors frame the server businesses of AMD and Intel. It is still unclear how quickly this demand will translate into EPYC and Xeon unit growth, but the direction of travel is already visible.

Enterprise spending on AI platforms is expanding the total addressable market for data center CPUs, even as accelerators dominate the spotlight.

AMD's current position marks a clear break from its long history of volatility. For much of the past two decades, its valuation moved within relatively narrow bands, interrupted by short-lived peaks during the Athlon and Opteron years.

Durable momentum only took hold after the launch of the Zen architecture in 2017, which reestablished AMD as a serious high-performance contender. Even then, investor confidence lagged. It was not until around 2020, when execution sharpened and the roadmap aligned with market demand, that the company's valuation began to move decisively.

Since then, AMD's growth has been closely tied to macro-level trends in compute. Its current valuation reflects not just product performance, but the expectation that it can capture a meaningful share of AI and cloud-driven infrastructure spending.

Intel's trajectory has been more complex. As recently as last August, its market cap had slipped below book value, a stark reflection of investor doubts around execution. The rebound followed a capital injection involving the US government, SoftBank, and Nvidia, reframing Intel as both a strategic domestic manufacturer and a potential beneficiary of AI demand. Its valuation today leans less on recent results and more on the belief that it can deliver competitive AI products at scale.

Arm sits in a different part of the stack. Traditionally focused on licensing its instruction set and core designs, the company has recently moved to producing its own data center-class CPUs.

But its real leverage lies elsewhere. Arm's ISA has become the default choice for hyperscalers designing custom silicon, giving it a foothold wherever cloud providers tailor hardware for specific AI workloads. Its reach across phones, tablets, vehicles, and now PCs makes it difficult to sidestep in any discussion about the future of compute.

Above them all is Nvidia, whose dominance in AI accelerators continues to anchor market expectations. The company was valued at about $4.8 trillion this week, not far from its October 2025 peak of roughly $4.92 trillion. That scale reflects more than demand for GPUs; it underscores Nvidia's position at the center of AI system design, where hardware, software, and interconnects are tightly coupled.

Taken together, the movement across these companies suggests a market increasingly organized around AI infrastructure. CPUs, GPUs, and custom silicon are no longer evaluated as standalone products but as interlocking parts of systems built for complex, data-intensive workloads. Current valuations imply that, in the eyes of investors, this shift is still closer to the beginning than the end.