Bottom line: Intel's next-generation 14A manufacturing technology is expected to deliver significant efficiency and performance improvements, but the company warns it will come at a higher price than its 18A process. Speaking at the Citi Global TMT Conference, chief financial officer David Zinsner cited the costly adoption of ASML's High-NA EUV lithography machines as the main factor behind the increased expense.

"14A is more expensive than 18A," Zinsner told investors. "It is a higher wafer cost, for sure and partly that is because we are expecting to use High-NA EUV tools in 14A, which was not the case in 18A."

Intel expects 14A to deliver power and performance advantages over 18A, including a 15 to 20 percent improvement in performance per watt or a 25 to 35 percent reduction in power consumption. These gains will come from several design changes. Among them are RibbonFET 2, Intel's updated gate-all-around transistor structure, and PowerDirect, a backside power delivery scheme that connects directly to the source and drain of transistors.

A standout feature of 14A is what Intel calls Turbo Cells – specialized double-height standard cells optimized for critical timing paths. By utilizing higher drive strength and compact layouts, Turbo Cells enable CPUs and GPUs manufactured using this process to achieve higher operating frequencies without incurring significant area or power penalties.

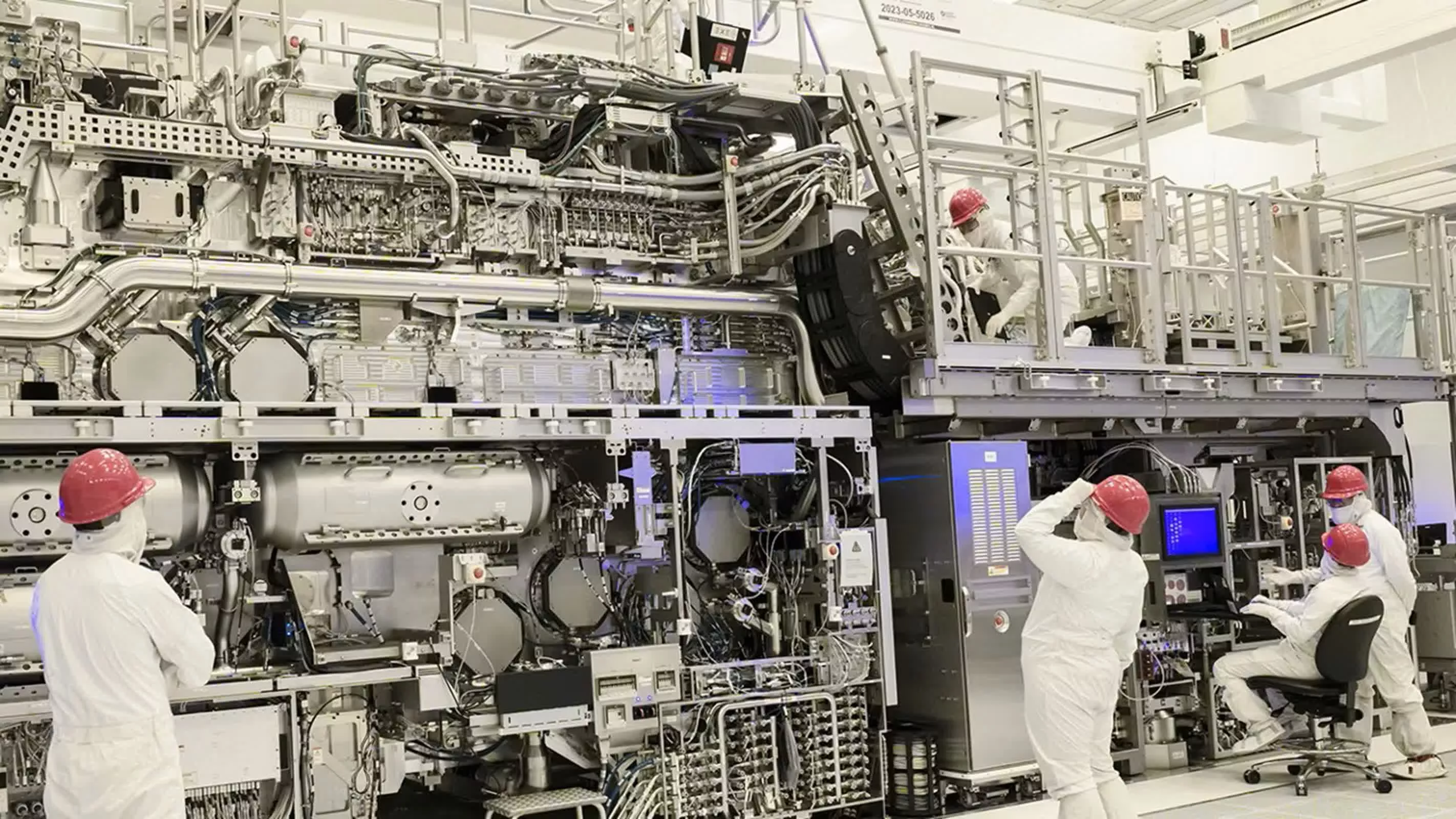

Unlike 18A, which can achieve its targets using multiple exposures on today's EUV systems, 14A requires ASML's High-NA EUV scanners to reach the resolution needed for future designs. These machines can pattern features down to 8 nanometers in a single pass compared to the 13.5 nm resolution of Low-NA tools. While conventional EUV can also achieve 8 nm through double patterning, that method adds complexity to the manufacturing process and can negatively affect chip yields.

ASML's High-NA EUV tools come at a steep price. The current Low-NA Twinscan NXE:3800E costs about $235 million per unit. Its successor, the EXE:5200B, will carry a price tag closer to $380 million per machine. For comparison, modern chip fabs designed for leading-edge processes already demand investments of between $20 billion and $30 billion, depending on their capacity. Adding several of the new machines to such facilities may not significantly alter overall capital costs, but 14A's development alone requires billions in research expenditures.

That combination of high R&D costs and expensive machine requirements makes 14A wafer production more costly than 18A. Intel is hoping its foundry clients will help shoulder that expense. "If we do not get 14A customers externally, it is going to be hard to justify that node," Zinsner said. While Intel's own products are guaranteed to use 14A, outside demand will be crucial in spreading costs and generating adequate returns for shareholders.

Earlier in 2025, Intel signaled that without a major foundry customer, it could slow or even cancel 14A altogether. The warning came at a time when the semiconductor industry has become increasingly wary of the staggering costs associated with bringing a new process node into production.

However, Intel may now have limited flexibility. The company's deal with the US government, which converted federal grants into equity, requires Intel to maintain at least 51 percent ownership of Intel Foundry for the next five years. Spinning off or winding down development of its fabrication arm would violate that agreement.

By contrast, TSMC has been more cautious about adopting High-NA technology. The company is waiting to determine whether the new tools provide enough value to offset their costs and integration challenges before deploying them broadly.

Intel, meanwhile, is making an aggressive bet that pushing forward with 14A and early adoption of High-NA EUV will give it a performance edge and enable key foundry customer wins. Whether that strategy creates enough demand to justify the costs remains one of the company's most pressing questions.

Image credit: PCMag